Income Tax Changes 2026 for Salaried Employees: HRA, Allowances & Real Salary Impact

Income tax changes 2026 for salaried employees impact HRA, allowance limits, and salary structure. Understand key updates and real tax implications.

Income Tax in India involves multiple rules covering tax slabs, deductions, filing requirements, and compliance obligations. This section provides plain-English guides curated by a Chartered Accountant, helping individuals and small business owners understand tax provisions with clear explanations, worked examples, and practical checklists.

You’ll find detailed guides on Old vs New Tax Regime comparisons, income tax slab rates, HRA exemption, standard deduction, and popular deductions such as Sections 80C, 80D, and 80G. The articles also explain taxation of salary income, house property, capital gains, and other income to help taxpayers calculate liability accurately.

Our guides also cover the ITR filing process (ITR-1 to ITR-3), key documents like Form 16, Form 26AS, AIS and TIS, and compliance topics including advance tax, self-assessment tax, TDS/TCS, interest under Sections 234A/B/C, and set-off of losses. Each article is regularly updated with Finance Act changes and CBDT circulars to help taxpayers plan better, avoid penalties, and file returns correctly.

If you’re looking for specific Income Tax topics in India, explore our most useful guides and tools below.

• Income Tax Calculator for AY 2026-27

• Old vs New Tax Regime Comparison

• Income Tax Slab Rates in India

• Section 80C, 80D & 80G Deductions Guide

• Capital Gains Tax Explained (LTCG & STCG)

• Form 16, AIS & Form 26AS Explained

• Advance Tax & Self-Assessment Tax Guide

• Interest under Sections 234A, 234B & 234C

• ITR Filing Guide (ITR-1 to ITR-3)

You can also explore our free Income Tax calculators and tools designed for quick tax estimation.

Income tax changes 2026 for salaried employees impact HRA, allowance limits, and salary structure. Understand key updates and real tax implications.

Can you claim HRA without paying rent? Understand the tax consequences, scrutiny risks, and what happens if your HRA claim is disallowed under the 2026 income tax framework.

Rent paid to parents HRA rules 2026 explained in simple terms. Understand eligibility, documentation, tax implications, and how to claim HRA safely under income tax rules 2026.

HRA calculation 2026 made simple with a real example. Understand the income tax rules 2026, exemption formula, salary definition, and how salaried employees can maximise tax savings through correct HRA calculation.

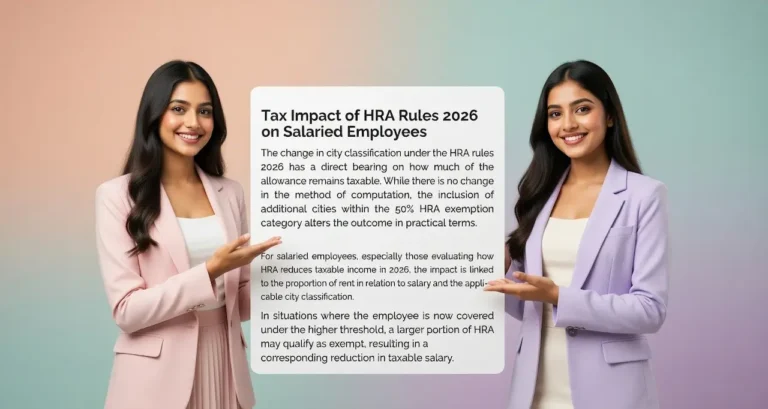

HRA rules 2026 bring a major tax advantage for salaried employees, with more cities now eligible for 50% exemption and stricter disclosure requirements. Understand how these income tax rules 2026 impact your HRA claim, documentation, and overall tax savings.

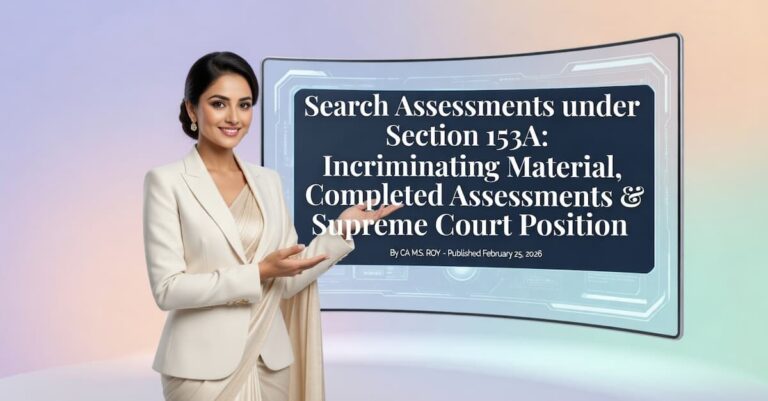

Can completed assessments be reopened after a search? Learn the Supreme Court ruling in Abhisar Buildwell on additions under Section 153A and the role of incriminating material.

Can completed assessments be reopened after search? This guide explains Section 153A incriminating material rule and the Supreme Court position in Abhisar Buildwell.

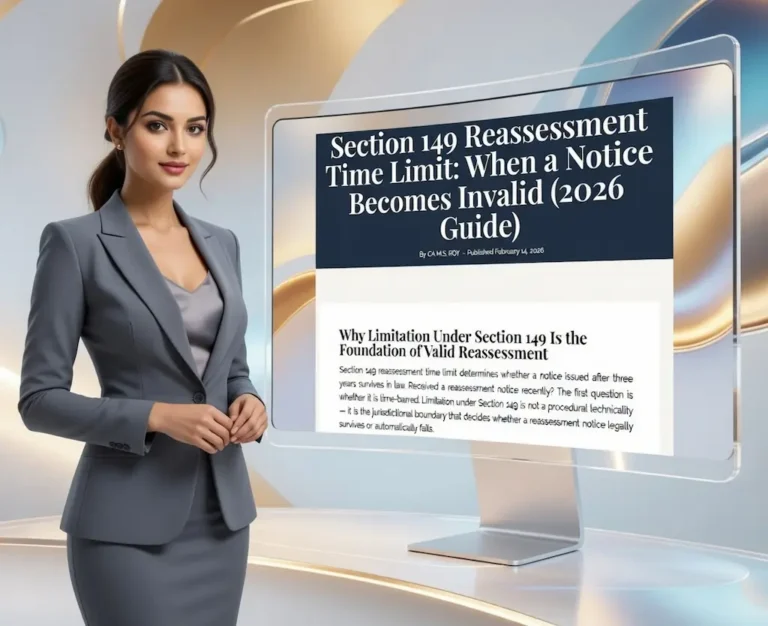

Received a reassessment notice after 3 years? The Section 149 reassessment time limit may determine whether the notice is legally valid or time-barred.

Reassessment fails when based on change of opinion. Learn how courts treat such notices as void despite section 148A and lack of fresh tangible material.

This FAQ section explains the income-tax proposals introduced in Union Budget 2026–27 under the theme of Attracting Global Business and Investment, with specific focus on data centre–related provisions. It covers tax exemptions for foreign companies, conditions applicable to specified data centres, and compliance requirements, helping readers understand the scope and intent of these measures.