Ensure GST Registration Compliance with the Right Documents

GST registration is governed by statutory requirements under the Central Goods and Services Tax Act, 2017.

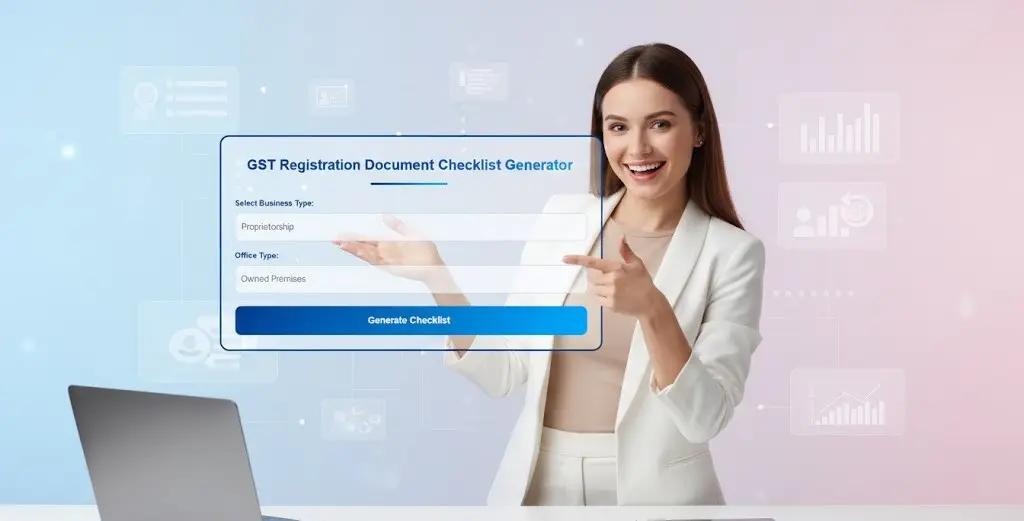

This GST Registration Document Checklist Tool helps identify the documents required for GST registration based on business constitution and principal place of business before filing Form GST REG-01.

Use this checklist as a pre-compliance verification step to avoid rejection or clarification notices.

GST Law Provisions Governing Registration Documents

GST registration is not merely a procedural formality. The requirement to furnish documents is rooted in statutory provisions that empower the tax authorities to verify the identity, existence, and place of business of the applicant.

Section 25 of the CGST Act, 2017

Section 25 mandates registration of persons liable under GST and authorises the proper officer to grant registration subject to conditions and restrictions as prescribed. The section forms the substantive legal foundation for registration under GST law.

Rule 8 of the CGST Rules, 2017

Rule 8 prescribes the filing of an application for registration in Form GST REG-01, along with documents and information as specified. The rule makes it clear that registration is conditional upon furnishing complete and correct particulars.

Rule 9 of the CGST Rules, 2017

Rule 9 empowers the proper officer to:

- Examine the application and documents

- Seek clarification where deficiencies are noticed

- Reject the application if the deficiencies are not rectified

In practice, most GST registration delays arise at this stage due to documentation issues, not eligibility.

Rule 10A and Aadhaar Authentication

Where applicable, Aadhaar authentication or physical verification becomes a precondition for approval of registration. Failure to comply can result in extended timelines or rejection.

📌 Compliance takeaway:

GST officers are legally empowered to scrutinise documents and reject applications where documentary evidence is inconsistent, outdated, or unverifiable.

Importance of Correct Documentation in GST Registration

From a professional compliance perspective, GST registration failures typically occur due to:

- Improper proof of principal place of business

- Mismatch between PAN, Aadhaar, and application data

- Absence of valid authorisation for the signatory

- Inadequate proof for rented or shared premises

- Old or unclear utility bills

Even eligible applicants face rejection when documents do not meet verification standards prescribed under the rules.

This checklist tool is designed to align document preparation with actual officer-level verification practices, not just theoretical requirements.

How the Checklist Is Determined

The document checklist is generated by evaluating two critical parameters that directly impact GST registration scrutiny.

1. Constitution of Business

GST law recognises different forms of business entities, each requiring specific documents and authorisations, such as:

- Proprietorship

- Partnership firm

- Limited Liability Partnership (LLP)

- Private or Public Limited Company

- Hindu Undivided Family (HUF)

- Trust / NGO

For example, a company requires board authorisation and constitutional documents, whereas a proprietorship relies primarily on proprietor identification and bank proof.

2. Principal Place of Business

Proof of place of business is a key verification area under GST registration. Documentation requirements differ depending on whether the premises is:

- Owned by the applicant

- Taken on rent or lease

- Shared or located in a co-working space

Incorrect address proof is one of the most frequent reasons for issuance of clarification notices under Rule 9.

How to Use This GST Document Checklist Tool

Using this tool is straightforward and requires only basic business details:

- Select the constitution of business

Choose the applicable business type such as proprietorship, partnership, LLP, company, HUF, or trust. - Select the principal place of business type

Indicate whether the business premises is owned, rented, or shared/co-working. - Generate the checklist

The tool will instantly display a customised list of documents commonly required for GST registration under the selected scenario. - Verify documents before filing Form GST REG-01

Use the generated checklist to ensure that all supporting documents are available, valid, and consistent before submitting the application on the GST portal.

📌 This tool is intended for pre-filing verification and should be used before initiating the GST registration process.

Practical Notes

In professional practice, GST registration rejections are rarely based on turnover thresholds or eligibility. They are usually caused by:

- Missing No Objection Certificates (NOC)

- Address proofs not matching application details

- Improper authorisation letters

- Unclear or outdated supporting documents

Using a structured checklist before filing Form GST REG-01 significantly reduces:

- Clarification notices

- Resubmissions

- Processing delays

This tool is therefore useful not only for business owners but also for Chartered Accountants, tax consultants, and GST practitioners handling multiple client registrations.

Scope and Limitations of This Tool

This tool provides a standardised GST registration document checklist based on statutory provisions and prevailing verification practices followed across India. It does not replace professional judgement, especially in cases involving:

- Special category States

- Multiple places of business

- Complex ownership structures

Professional review is recommended prior to final submission on the GST portal.

Frequently Asked Questions

Is this checklist legally sufficient for GST registration?

It covers standard statutory and procedural requirements but should be reviewed against specific facts of each case.

Does this tool file GST registration on the portal?

No. The tool only assists in identifying required documents.

Can professionals rely on this tool for client work?

Yes. It can be used as a preliminary compliance and verification checklist.

Is the checklist aligned with current GST practice?

Yes. It reflects prevailing registration scrutiny practices followed by GST authorities.