Calculate MGT-7 Late Filing Fee

Compute the exact MGT-7 penalty based on the due date and actual filing date. The tool automatically calculates ₹100 per day with no maximum cap.

MGT-7A Penalty for Small Companies & OPC

Check late filing fee for MGT-7A applicable to OPC and Small Companies. Enter the delay period and get instant ROC additional fee calculation.

Accurate ₹100 Per Day Computation

Under Section 403 of the Companies Act, additional fee is ₹100 per day of delay. Use this MGT-7 penalty calculator to avoid errors and surprises.

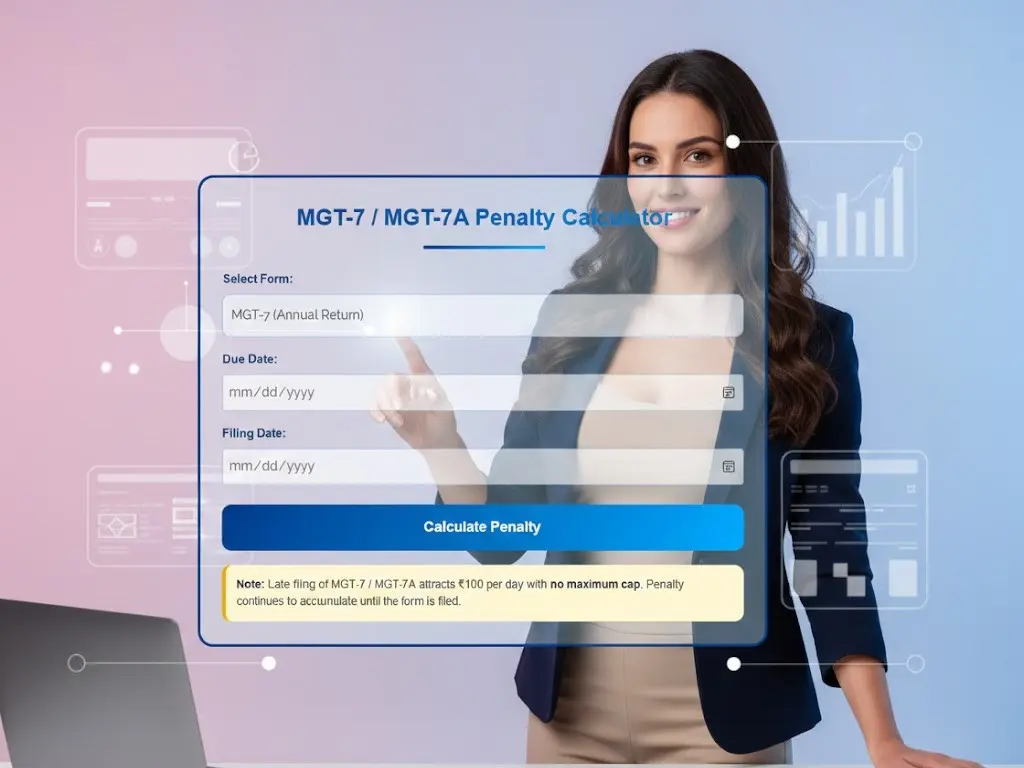

What This MGT-7 / MGT-7A Penalty Calculator Does

The MGT-7 / MGT-7A Penalty Calculator is designed to help companies instantly compute the late filing fee payable for delayed filing of annual return under the Companies Act, 2013. If you are searching for a reliable MGT-7 penalty calculator or MGT-7 late filing fee calculator, this tool gives you an accurate computation based on statutory rules.

Under Section 403 of the Companies Act, delay in filing Form MGT-7 or MGT-7A attracts an additional fee of ₹100 per day, with no maximum cap. Even a small delay can significantly increase compliance cost.

This MGT-7A penalty calculator automatically: Calculates total delay days. Its applies ₹100 per day additional fee, Computes total late filing fee payable to MCA.

It eliminates manual counting errors and helps professionals determine the exact MGT-7 late filing fee before submitting the form on the MCA portal.

How the MGT-7 / MGT-7A Penalty is Calculated

The MGT-7 / MGT-7A Penalty Calculator computes the number of days of delay between the statutory due date and the actual filing date and applies the additional fee prescribed under Section 403 of the Companies Act, 2013.

As per the MCA framework, late filing of annual return attracts an additional fee of ₹100 per day of delay, with no maximum cap. This means the total late filing fee increases proportionately for every day the form remains unfiled after the due date.

The formula applied by this calculator is straightforward:

Delay Days × ₹100 = Total Additional Fee Payable. This helps companies and professionals determine the exact MGT-7 or MGT-7A late filing fee before proceeding with ROC filing on the MCA portal.

What is Form MGT-7 and MGT-7A?

Form MGT-7 is the Annual Return required to be filed under Section 92 of the Companies Act, 2013 by every company, except where a simplified return is permitted. It is a comprehensive statutory document that captures key information about the company’s structure and compliance status as on the close of the financial year. The return includes details relating to registered office, principal business activities, share capital structure, shareholding pattern, directors and key managerial personnel, indebtedness, and other corporate disclosures.

Form MGT-7A is a simplified annual return introduced for One Person Companies (OPC) and Small Companies. While the disclosure requirements are comparatively reduced, the legal obligation to file the return within the prescribed timeline remains mandatory. Both MGT-7 and MGT-7A serve as critical compliance filings with the Registrar of Companies (ROC), and delay in filing attracts additional fees under the Companies Act.

Failure to file the annual return within the statutory period triggers late filing fee under Section 403, which is calculated at ₹100 per day of delay. This is the basis on which the MGT-7 / MGT-7A Penalty Calculator determines the additional fee payable.

MGT-7 / MGT-7A Due Date Explained

Under Section 92(4) of the Companies Act, 2013, every company is required to file its annual return within sixty days from the date of the Annual General Meeting (AGM). In practical terms, if the AGM is held on 30 September, the due date for filing Form MGT-7 or MGT-7A would generally fall 60 days thereafter.

Even where the AGM is not held, the obligation to file the annual return does not disappear. The company must file the return within sixty days from the date on which the AGM should have been held in accordance with the Act. Therefore, non-holding of AGM does not extend the filing timeline indefinitely.

Once the statutory due date is crossed, additional filing fee becomes payable at the rate prescribed under Section 403. Since there is no maximum cap on the late filing fee, the liability increases proportionately with each day of delay. Accurate calculation of the delay period is therefore essential to estimate the total amount payable before filing the form on the MCA portal.

Late Filing Fees under the Companies Act – Section 403 Explained

Late filing of Form MGT-7 or MGT-7A attracts additional fee under Section 403 of the Companies Act, 2013. The provision states that where a document is not filed within the prescribed time, it may still be filed with payment of such additional fee as may be prescribed. In the case of annual return forms, the Ministry of Corporate Affairs (MCA) has prescribed an additional fee of ₹100 per day of delay.

Importantly, there is no maximum cap on the additional fee for delayed filing of MGT-7 or MGT-7A. This means the late filing fee continues to increase for every day the form remains unfiled beyond the due date. Even a delay of a few months can result in a substantial compliance cost.

It is also important to distinguish between “additional fee” and “penalty.” The ₹100 per day amount is an additional filing fee payable at the time of submission of the form. Separate penalties or prosecution consequences may arise in cases of prolonged or intentional non-compliance under other provisions of the Act.

For compliance planning purposes, accurate estimation of the additional fee is critical. This is where the MGT-7 / MGT-7A Penalty Calculator becomes useful, as it computes the exact amount payable based on the number of days of delay.

Difference Between MGT-7 and MGT-7A

While both forms relate to filing of annual return under Section 92, their applicability differs based on the category of company. Form MGT-7 is applicable to most companies, including private limited companies and public companies that do not fall within the definition of Small Company or OPC. It requires detailed disclosures relating to shareholding pattern, indebtedness, directors, promoters and compliance matters.

Form MGT-7A, on the other hand, is a simplified annual return introduced for One Person Companies (OPC) and Small Companies as defined under the Companies Act

The simplified form reduces disclosure requirements but does not reduce compliance responsibility. The due date and the additional fee structure remain the same. Therefore, delay in filing MGT-7A also attracts ₹100 per day of delay without any maximum ceiling.

Understanding the distinction is important before using the MGT-7 / MGT-7A late filing fee calculator, as the form selected should correspond to the company’s legal status.

Consequences of Non-Filing of MGT-7 / MGT-7A

Non-filing or prolonged delay in filing Form MGT-7 or MGT-7A can lead to consequences beyond payment of additional fee under Section 403. While the immediate financial impact is the ₹100 per day late filing fee, continued non-compliance may expose the company and its officers to penal provisions under the Companies Act, 2013.

Section 92 provides that failure to file the annual return may attract penalties on the company as well as every officer in default. In serious cases, the Registrar of Companies (ROC) may initiate adjudication proceedings, issue show-cause notices, or take further regulatory action. Persistent non-compliance can also affect the company’s compliance record and corporate standing.

Additionally, failure to maintain timely statutory filings may create complications during:

Bank due diligence

Investor funding rounds

Statutory audits

Corporate restructuring or strike-off proceedings

For these reasons, companies should not treat MGT-7 or MGT-7A as a routine filing. Monitoring the due date and estimating potential late filing fee in advance using the MGT-7 penalty calculator helps avoid unexpected compliance costs and regulatory exposure.

Frequently Asked Questions (FAQs) on MGT-7 / MGT-7A Late Filing Fee

Related Company Act Compliance Tools

Looking for more ROC and MCA compliance calculators? You may also find these tools useful:

- AOC-4 Late Filing Penalty Calculator – Calculate additional fee for delayed financial statement filing

- MCA Late Filing Fee Calculator – Compute general ROC additional filing charges

- SPICe+ Incorporation Checklist Generator – Step-by-step checklist for company incorporation

- Company Incorporation Cost Estimator – Estimate MCA fees and professional costs

- Authorised Share Capital Fee Calculator – Calculate government filing fees based on capital structure

Explore the complete Company Act Tools Suite for more compliance calculators.

Disclaimer: The late filing fee is computed based on Section 403 of the Companies Act, 2013. Users should confirm the final payable amount from the MCA system before submission.