INTRODUCTION

From April 2026, HRA rules are set to change under the income tax rules 2026, and this could directly impact how much tax you pay on your salary.

For many salaried employees, House Rent Allowance (HRA) is one of the biggest components used to reduce taxable income. With the latest updates, the government has expanded eligibility, increased effective exemption benefits, and tightened compliance requirements.

But here’s the catch — most people will only look at the headline changes and miss the real opportunity to save more tax.

In this guide, we break down the HRA rules 2026, explain what has changed compared to earlier provisions, and most importantly, show how it impacts your salary and tax savings with practical examples.

What Changed in HRA Rules 2026?

If you are a salaried employee paying rent, the HRA rules 2026 can directly affect your tax.

The basic formula for HRA calculation is still the same.

But under the income tax rules 2026, the real change is in who can claim higher exemption and how strictly it is checked.

Earlier, higher HRA exemption (50% of salary) was mostly limited to metro cities.

Now, because rents have increased in many cities, more employees may effectively qualify for a higher exemption.

At the same time, the government has tightened the rules to ensure that HRA claims are genuine and properly supported.

So, while the structure remains the same, the benefit has increased — but compliance has also become stricter.

To understand this better, here are the key changes you should know:

- More employees may qualify for higher HRA exemption in 2026

- The benefit now depends more on actual rent and city classification

- Proper landlord details and documentation are required

- Incorrect or unsupported HRA claims may be disallowed

If you are a salaried employee paying rent, you may now qualify for a higher HRA exemption — but only if your claim is correct and properly documented.

HRA Calculation 2026

There is no change in the method of computing HRA exemption.

The exemption continues to be determined on the basis of three standard parameters — salary, rent paid, and place of residence. The least of the prescribed values is treated as exempt, and the balance forms part of taxable income.

The computation remains as follows:

- Actual HRA received

- Rent paid in excess of 10% of salary

- 50% of salary (for specified cities) or 40% in other cases

The lowest of the above is allowed as exemption.

In practice, the calculation is straightforward but often misunderstood.

The exemption is not linked to the full amount of HRA received. It depends on how rent compares with salary and whether the location qualifies for the higher percentage threshold.

Illustration

Consider the following:

- Basic salary (including DA, where applicable): ₹50,000 per month

- HRA received: ₹20,000 per month

- Rent paid: ₹18,000 per month

The calculation would be:

- Actual HRA: ₹20,000

- Rent minus 10% of salary: ₹18,000 – ₹5,000 = ₹13,000

- 50% of salary: ₹25,000

The exemption is restricted to ₹13,000 per month, being the lowest of the above. The remaining HRA is taxable.

The position remains unchanged under the current framework. However, as discussed earlier, the relevance of this calculation has increased due to higher rental values and broader applicability.

HRA Exemption Cities List 2026 (50% vs 40% Classification)

One of the key updates under the HRA rules 2026 is the expansion of cities eligible for higher exemption.

Earlier, the benefit of 50% of salary for HRA exemption was limited to four metro cities — Delhi, Mumbai, Chennai and Kolkata. All other locations were covered under the 40% limit, even where rent levels were high.

Under the updated position reflected in the income tax rules 2026, this scope has been widened. A few large cities have now been included in the higher exemption category, recognising the increase in rental costs.

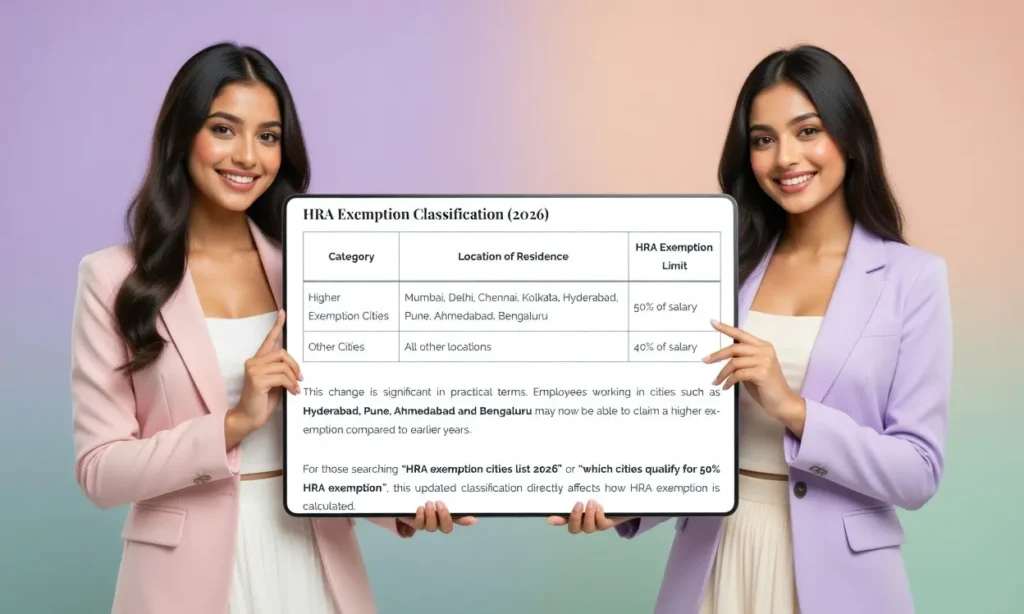

To understand the current position clearly, the classification can be summarised as follows:

HRA Exemption Classification (2026)

| Category | Location of Residence | HRA Exemption Limit |

|---|---|---|

| Higher Exemption Cities | Mumbai, Delhi, Chennai, Kolkata, Hyderabad, Pune, Ahmedabad, Bengaluru | 50% of salary |

| Other Cities | All other locations | 40% of salary |

This change is significant in practical terms. Employees working in cities such as Hyderabad, Pune, Ahmedabad and Bengaluru may now be able to claim a higher exemption compared to earlier years.

For those searching “HRA exemption cities list 2026” or “which cities qualify for 50% HRA exemption”, this updated classification directly affects how HRA exemption is calculated.

Key takeaway

- More cities now fall under the 50% HRA exemption category

- Employees in these cities may get higher tax-free HRA

- The benefit depends on salary, rent paid and correct classification

What This Means for Salaried Employees

The expansion of cities is not just a classification change. It has a direct effect on how much of your HRA becomes tax-free.

For many salaried employees, especially those paying higher rent, this change can improve the overall tax position without any change in salary structure.

To understand the impact better, it helps to look at how this affects real situations:

- Employees in newly added cities may now fall under the higher exemption category

- A larger portion of HRA may qualify as tax-free income

- The taxable part of salary may reduce, even if salary remains unchanged

In practical terms, if you are paying rent in cities like Pune, Bengaluru or Hyderabad, the updated rules may result in higher HRA exemption in 2026, depending on your rent and salary.

This is why many are now searching for “HRA benefit for salaried employees 2026” or “how HRA reduces taxable income”.

Key takeaway for employees

- Same salary → better utilisation of HRA exemption

- Higher rent → greater tax benefit

- Correct classification → lower taxable income

At the same time, the benefit is not automatic. It depends on correct calculation and proper documentation, which becomes important in the later sections.

Tax Impact of HRA Rules 2026 on Salaried Employees

The change in city classification under the HRA rules 2026 has a direct bearing on how much of the allowance remains taxable. While there is no change in the method of computation, the inclusion of additional cities within the 50% HRA exemption category alters the outcome in practical terms.

For salaried employees, especially those evaluating how HRA reduces taxable income in 2026, the impact is linked to the proportion of rent in relation to salary and the applicable city classification.

In situations where the employee is now covered under the higher threshold, a larger portion of HRA may qualify as exempt, resulting in a corresponding reduction in taxable salary.

To understand the practical effect, the following points may be noted:

- employees located in cities now covered under 50% HRA exemption may see higher exempt amounts

- where rent constitutes a significant part of salary, the benefit becomes more pronounced

- the taxable portion of HRA may reduce even without any change in salary structure

The overall saving will vary from case to case. However, for those paying market-level rent, the revised position under the income tax rules 2026 makes HRA a more relevant component in tax computation.

Conditions to Claim HRA Exemption in 2026

The conditions governing HRA exemption continue to apply in the same manner. There is no substantive change in eligibility; however, correct application of these conditions remains essential while determining how to claim HRA exemption in 2026.

The exemption is not available automatically. It is linked to actual facts and must be computed in accordance with the prescribed method.

For clarity, the key requirements are as follows:

- HRA must form part of the salary received by the employee

- the employee should incur expenditure on rent for residential accommodation

- the accommodation occupied should not be owned by the employee

In addition to the above, certain practical aspects require attention:

- where no rent is paid, HRA is fully taxable

- the exemption is restricted to the amount calculated, not the entire HRA received

- claims should be capable of verification based on supporting records

These aspects are particularly relevant for those reviewing HRA rules for salaried employees 2026 or assessing eligibility before claiming exemption.

The current framework places greater emphasis on accuracy and consistency in reporting, rather than altering the underlying conditions.

Rent Paid to Parents — Tax Position in 2026

Rent paid to parents continues to qualify for HRA exemption, provided the arrangement is genuine. There is no restriction under the law on claiming exemption in such cases. However, under the current framework, greater emphasis is placed on verifiable transactions and proper disclosure, particularly where the landlord is a related person.

For salaried employees reviewing “can HRA be claimed if rent is paid to parents in 2026” or “HRA rules for rent paid to family members”, the position remains permissible but subject to closer scrutiny.

In practice, the following aspects become relevant:

- rent should be actually paid, preferably through banking channels

- the parent receiving rent should report it as income in the return of income

- the arrangement should reflect a genuine tenancy and not a notional claim

Where these conditions are not met, the exemption may be questioned during assessment or verification.

The intent is not to disallow such claims, but to ensure that they reflect real transactions and are capable of being substantiated.

Documentation and Compliance Requirements

While the basic conditions for HRA remain unchanged, the approach to documentation has become more structured under the income tax rules 2026. The emphasis is on ensuring that claims are supported by consistent and verifiable records.

This is particularly relevant for those reviewing documents required for HRA exemption in 2026 or HRA compliance rules in India, as incomplete or inconsistent records may lead to disallowance.

From a practical standpoint, the following should be maintained:

- rent receipts or other proof of payment

- landlord details, including PAN where applicable

- consistency between rent claimed and salary records

IA further aspect that assumes importance is disclosure, especially where rent is paid to a related person.

In such cases, the employee may be required to indicate the relationship with the landlord and provide supporting details, as may be called for by the employer or during verification.

This is relevant in the context of HRA disclosure requirements 2026, particularly on the question of whether the relationship with the landlord needs to be reported.

The underlying position remains unchanged; however, the current framework places greater reliance on accuracy, consistency and transparency in reporting, rather than introducing new conditions.

Common Mistakes in HRA Claims

Errors in HRA claims are usually not due to complexity of law, but due to incorrect understanding or casual documentation. Under the current framework, such mistakes are more likely to be identified.

For those reviewing common mistakes in HRA exemption claims or why HRA gets disallowed, the following areas require attention:

- treating the entire HRA received as tax-free, without applying the prescribed calculation

- claiming HRA without actual payment of rent

- paying rent in cash without maintaining proper records

- claiming rent paid to parents without corresponding income disclosure by the parent

- mismatch between rent claimed and salary details reported

These issues generally arise at the time of employer verification or during assessment. The emphasis is not on restricting claims, but on ensuring that they are factually correct and supported by evidence.

HRA and New Tax Regime — Position in 2026

The availability of HRA exemption continues to depend on the tax regime opted by the employee.

Under the old tax regime, HRA exemption is available subject to the prescribed conditions. However, under the new tax regime, HRA is not allowed as an exemption.

This becomes relevant for employees evaluating old vs new tax regime for salaried employees 2026 or assessing whether to continue claiming HRA.

From a practical standpoint:

- old regime → HRA exemption available

- new regime → HRA fully taxable

Accordingly, employees receiving substantial HRA and paying significant rent may find the old regime more favourable, subject to overall tax computation.

Conclusion

The HRA rules 2026 do not alter the method of computation, but they do change the practical relevance of the exemption.

With the inclusion of additional cities under the higher exemption category and increased emphasis on documentation and disclosure, HRA assumes greater importance in salary taxation.

For salaried employees, the benefit lies not in the rule itself, but in correct application and proper reporting.

FAQs

What is HRA exemption in 2026?

HRA exemption is the portion of House Rent Allowance that is exempt from tax, calculated as per prescribed conditions under the income tax rules.

Which cities qualify for 50% HRA exemption in 2026?

Mumbai, Delhi, Chennai, Kolkata, Hyderabad, Pune, Ahmedabad and Bengaluru fall under the higher exemption category.

Can HRA be claimed if rent is paid to parents?

Yes, HRA can be claimed if rent is paid to parents, provided the arrangement is genuine and the income is reported by the parent.

Is HRA allowed in the new tax regime?

No, HRA exemption is not available under the new tax regime.

What documents are required for HRA exemption?

Rent receipts, landlord details (including PAN where applicable), and proof of rent payment are generally required.

You may also like

- HRA Calculation Explained with Examples (2026 Guide)

- Old vs New Tax Regime for Salaried Employees: Which One to Choose in 2026

- Salary Structure Planning: How to Maximise Tax Savings Legally

- Can You Claim HRA and Home Loan Together? Complete Guide

- Rent Paid to Parents: Tax Implications and Compliance Requirements

- Top Tax Saving Options for Salaried Employees Beyond Section 80C

Try HRA Calculation Tool

For a quick and accurate estimate, you can use our HRA Calculator for 2026 to check how much exemption you can claim based on your salary, rent and city.

👉 Calculate here: HRA Exemption Calculator AY 2026-27 – Know Taxable HRA Instantly

Sources and References

- Income-tax Act, 1961 — provisions relating to House Rent Allowance

- Income Tax Rules, 1962 and updates under Income Tax Rules 2026

- Income-tax Act 2025

- Income Tax Rules, 2026

- Government notifications and official clarifications issued from time to time

Disclaimer

This article is intended for general informational purposes based on the provisions relating to HRA rules 2026 and the applicable framework under the Income-tax law. The position discussed is of a general nature and may vary depending on individual facts, salary structure and interpretation of rules.

Readers are advised to verify the applicability in their specific case or consult a professional before taking any decision.