Introduction

Rent paid to parents HRA rules 2026 have become an important area of discussion for salaried employees evaluating tax saving options. The question of whether HRA can be claimed on rent paid to parents has gained renewed attention under the income tax rules 2026. For many salaried employees, this is not just a tax planning strategy but a practical arrangement, especially when living in a family-owned house.

While the law does permit such claims, the real issue lies in understanding the conditions and compliance expectations attached to it. With increased focus on disclosure and verification, the manner in which HRA is claimed has become as important as the eligibility itself.

A clear understanding of the legal position, documentation requirements and tax implications is essential to ensure that the claim is both valid and sustainable.

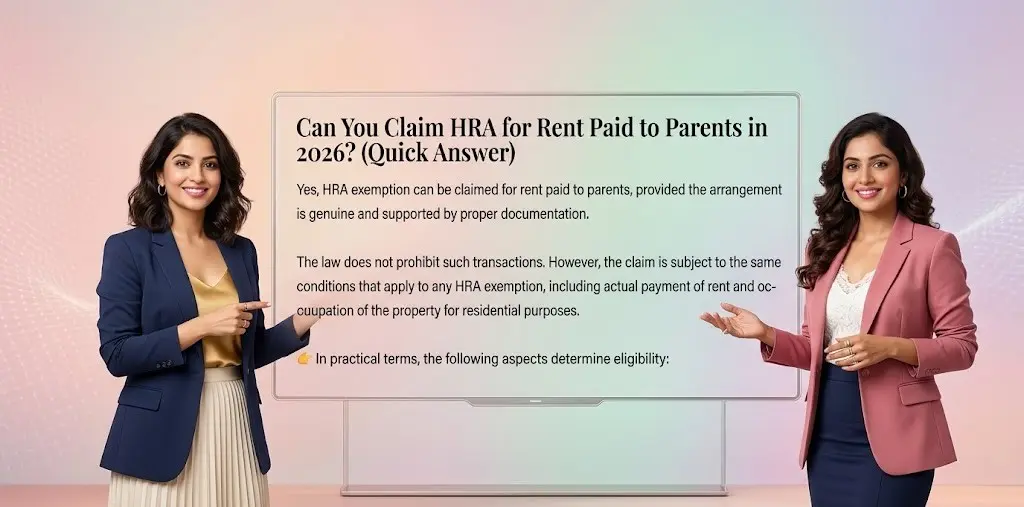

Can You Claim HRA for Rent Paid to Parents in 2026? (Quick Answer)

Yes, HRA exemption can be claimed for rent paid to parents, provided the arrangement is genuine and supported by proper documentation.

The law does not prohibit such transactions. However, the claim is subject to the same conditions that apply to any HRA exemption, including actual payment of rent and occupation of the property for residential purposes.

👉 In practical terms, the following aspects determine eligibility:

- rent must be actually paid and not merely recorded

- parents should be the legal owners of the property

- the arrangement should reflect a real landlord-tenant relationship

The allowance of such claims continues under the current framework, but with a greater emphasis on verification. Accordingly, while the benefit remains available, the burden of proof has become more significant under the income tax rules 2026.

Legal Position Under Income Tax Law: What the Rules Actually Say

HRA exemption is governed by the provisions relating to salary income, and there is no restriction in the law that disallows exemption merely because rent is paid to parents.

Under the earlier framework as well as the current structure, the focus has always been on whether the employee has actually incurred expenditure on rent. The identity of the landlord, by itself, is not a disqualifying factor.

👉 The legal position can be understood through the following principles:

- HRA exemption is linked to actual rent payment, not relationship

- ownership of the property must lie with the person receiving rent

- the transaction should be capable of verification

In essence, the law recognises such arrangements, but only where they reflect genuine transactions and are supported by consistent records.

What Changed in 2026: 1962 Rules vs Current Framework

The transition from the Income Tax Rules, 1962 to the Income Tax Rules, 2026 does not alter the eligibility of claiming HRA on rent paid to parents. However, the framework reflects a shift towards greater transparency and verification.

Under the earlier rules, claims were largely accepted where basic documentation was available. The current framework places greater emphasis on consistency of reporting and genuineness of transactions, particularly in related-party arrangements.

👉 The key changes can be summarised as follows:

- continued eligibility for HRA on rent paid to parents

- increased focus on verification and audit trail of transactions

- emphasis on disclosure where landlord is a related person

- closer alignment between employer records and tax filings

In effect, while the law remains unchanged, the level of scrutiny has increased under the income tax rules 2026.

Key Conditions to Claim HRA for Rent Paid to Parents

The ability to claim HRA in such cases depends not on relationship, but on whether the transaction satisfies the prescribed conditions.

For those evaluating rent paid to parents HRA rules 2026, the following conditions are critical in practice:

- rent must be actually paid and not merely recorded

- parents must be the legal owners of the property

- the property should be used for residential purposes

- the arrangement should reflect a genuine landlord-tenant relationship

These conditions are not new, but their correct application is essential. Failure to meet any of these may result in disallowance of exemption.

The emphasis under the current framework is on substance over form, ensuring that the claim reflects a real transaction rather than a tax arrangement.

Documentation and Disclosure Requirements (2026 Focus)

Documentation assumes greater importance under the income tax rules 2026, particularly in cases involving rent paid to parents. The claim must be supported by records that are consistent and capable of verification.

For employees reviewing documents required for HRA rent paid to parents, the following should be maintained:

- rent receipts or proof of payment

- landlord details, including PAN where applicable

- rental agreement, where feasible

- evidence of payment through banking channels

In addition to documentation, disclosure has become a key requirement. Where rent is paid to a related person, the relationship may need to be indicated and supported with appropriate details.

The focus is not on restricting claims, but on ensuring that they are accurate, transparent and verifiable.

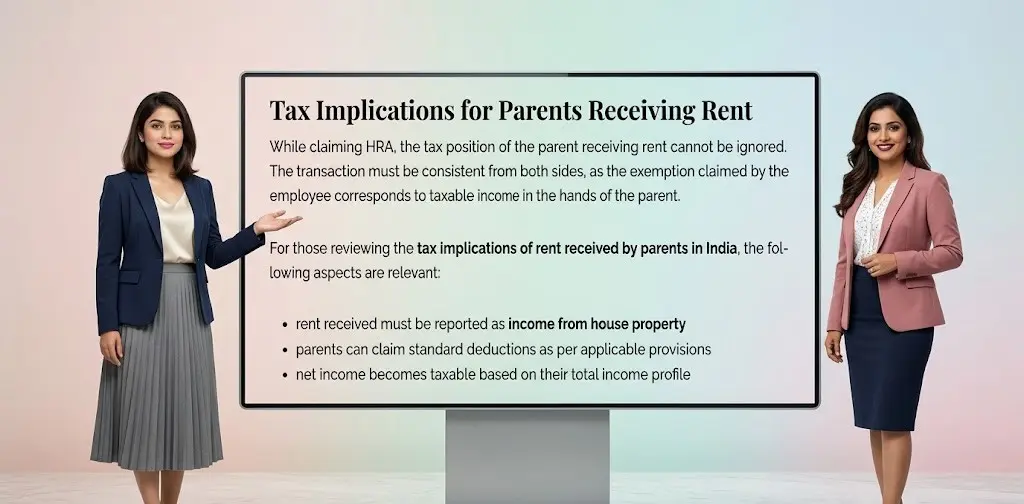

Tax Implications for Parents Receiving Rent

While claiming HRA, the tax position of the parent receiving rent cannot be ignored. The transaction must be consistent from both sides, as the exemption claimed by the employee corresponds to taxable income in the hands of the parent.

For those reviewing the tax implications of rent received by parents in India, the following aspects are relevant:

- rent received must be reported as income from house property

- parents can claim standard deductions as per applicable provisions

- net income becomes taxable based on their total income profile

Where the parent falls in a lower tax bracket, the overall tax impact may still be beneficial at a family level.

Accordingly, while HRA can reduce taxable salary, the corresponding taxability in the hands of parents must be considered to ensure consistency and compliance.

When HRA Claims May Be Disallowed (High-Risk Situations)

Although HRA can be claimed for rent paid to parents, such claims are more likely to be examined where the arrangement lacks substance.

For employees evaluating when HRA claims may be disallowed in 2026, certain situations carry higher risk.

👉 The following cases may lead to disallowance:

- no actual payment of rent or only notional entries

- cash payments without supporting evidence

- property effectively owned or controlled by the employee

- mismatch between rent claimed and income declared by parents

- absence of documentation or inconsistent records

These situations raise questions on the genuineness of the transaction. Under the current framework, there is greater emphasis on verifiable and consistent reporting, especially in related-party cases.

Practical Example: HRA Claim with Rent Paid to Parents

A practical illustration helps in understanding how the rules operate in real situations.

Consider a case where an employee pays rent to parents for residing in their property.

- Basic Salary: ₹50,000 per month

- HRA received: ₹20,000 per month

- Rent paid to parents: ₹15,000 per month

Applying the standard HRA calculation method:

- actual HRA received

- rent paid minus 10% of salary

- applicable percentage of salary based on city

The exemption will be the lowest of the above values.

If the rent is actually paid, properly documented, and reported as income by the parents, the HRA claim is generally sustainable.

This example highlights that the allowability of HRA depends on correct calculation and genuine transaction, rather than the relationship with the landlord.

Rent Paid to Parents vs Own House: Key Distinction

A common area of confusion arises where employees reside in a property owned by their parents but do not have a clear rental arrangement. The distinction between a genuine tenancy and self-occupation is critical for HRA purposes.

For those evaluating whether HRA is allowed for parents’ house in India, the following distinction becomes relevant:

- HRA is allowed where rent is actually paid to parents as owners

- HRA is not available where the employee owns the property

- mere residence in a family house without rent payment does not qualify

The key factor is the existence of a genuine rental transaction, supported by payment and documentation. The relationship, by itself, does not determine eligibility.

Common Mistakes and Compliance Risks

Errors in claiming HRA for rent paid to parents generally arise from incorrect assumptions rather than legal restrictions.

For employees reviewing common mistakes in HRA claims 2026, the following areas require attention:

- assuming that relationship automatically allows exemption

- claiming rent without actual payment

- not reporting corresponding income in parents’ return

- lack of documentation or inconsistent records

- ignoring disclosure requirements in related-party transactions

Such issues may lead to disallowance or queries during assessment. The current framework places emphasis on accuracy, transparency and consistency across filings.

Conclusion

The rent paid to parents HRA rules 2026 continue to allow exemption, provided the arrangement is genuine and properly documented. The law does not restrict such claims, but the compliance expectations have become more structured.

For salaried employees, the focus should be on substance of transaction, correct calculation and proper disclosure, rather than merely meeting formal conditions.

FAQs

Can I claim HRA if I pay rent to parents in 2026?

Yes, HRA can be claimed if rent is paid to parents, provided the arrangement is genuine and supported by documentation.

Is rent paid to parents taxable for them?

Yes, rent received by parents is taxable as income from house property.

Is disclosure required for rent paid to parents?

Yes, where applicable, the relationship with the landlord may need to be disclosed and supported with records.

Can HRA be claimed if I live in my own house?

No, HRA exemption is not available if the employee resides in a self-owned property.

What documents are required for HRA rent to parents?

Rent receipts, landlord details, and proof of payment are generally required.

Further Reading

For a better understanding of HRA provisions and their practical application, the following related guides may be useful:

- HRA Rules 2026 Explained: Higher Exemption, New Cities & Salary Impact

- HRA Calculation 2026 With Example: Save Tax Using Latest Rules

- Old vs New Tax Regime 2026: Should Salaried Employees Claim HRA?

Sources and References

- Income-tax Act, 1961 — provisions relating to salary income and HRA (Section 10(13A))

- Income Tax Rules, 1962 — earlier framework governing HRA computation (Rule 2A)

- Income Tax Rules, 2026 — restructured rules and updated compliance framework

- Income-tax Act, 2025

- Government notifications and official releases relating to salary taxation and HRA

Disclaimer

This article provides general guidance on rent paid to parents HRA rules 2026 based on the applicable provisions under the income tax law. The position discussed is of a general nature and may vary depending on individual facts, documentation and interpretation of rules.

Readers are advised to verify the applicability in their specific case or consult a professional before taking any decision. The law and its interpretation may be subject to further clarification or updates.