Introduction

HRA calculation 2026 is one of the most important aspects of tax planning for salaried employees. House Rent Allowance (HRA) continues to be a practical way to reduce taxable income under the income tax rules 2026.

With the introduction of the updated framework, there is renewed interest in understanding how HRA exemption works in practice and whether any changes have a real impact on tax savings. While the method of calculation remains unchanged, the effect has become more meaningful due to changes in city classification and increased compliance focus.

A clear understanding of HRA calculation 2026 not only helps avoid errors but also enables salaried employees to maximise tax savings under the old tax regime.

Understanding HRA Exemption Under Income Tax Rules 2026

HRA exemption is governed by the provisions relating to salary income and continues to be available to employees who pay rent for residential accommodation. Under the income tax rules 2026, the structure of the law has been reorganised, but the basic principle remains unchanged.

In practical terms, HRA is a part of salary, but only a portion of it is exempt from tax, subject to prescribed conditions. This exemption is not automatic and depends on factors such as salary, rent paid, and place of residence.

For employees searching how to claim HRA exemption in 2026, it is important to note that eligibility continues only under the old tax regime, and proper documentation remains essential.

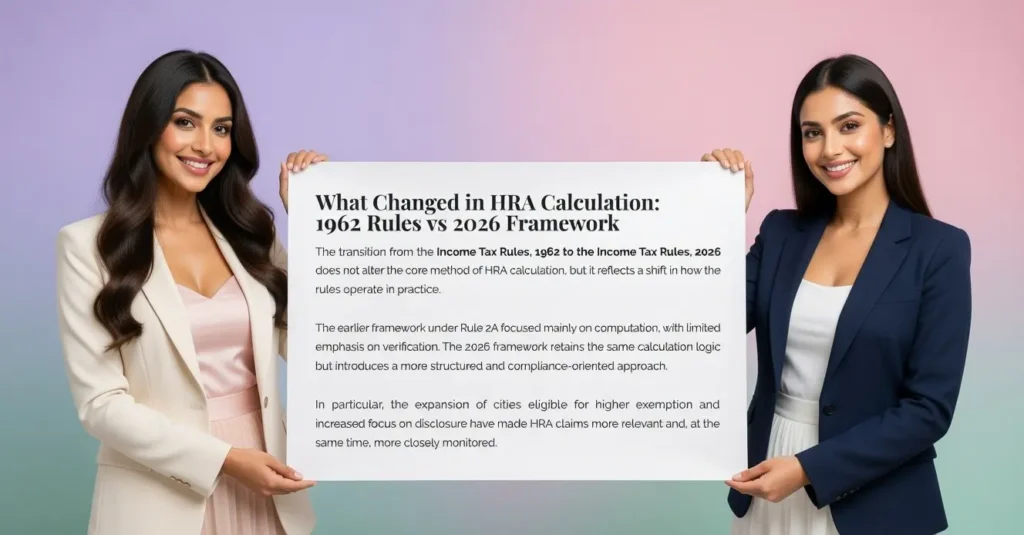

What Changed in HRA Calculation: 1962 Rules vs 2026 Framework

The transition from the Income Tax Rules, 1962 to the Income Tax Rules, 2026 does not alter the core method of HRA calculation, but it reflects a shift in how the rules operate in practice.

The earlier framework under Rule 2A focused mainly on computation, with limited emphasis on verification. The 2026 framework retains the same calculation logic but introduces a more structured and compliance-oriented approach.

In particular, the expansion of cities eligible for higher exemption and increased focus on disclosure have made HRA claims more relevant and, at the same time, more closely monitored.

In essence, while the formula remains unchanged, the tax impact and compliance expectations have evolved.

HRA Calculation Formula 2026 (Step-by-Step Method)

The method of HRA calculation under the income tax rules 2026 continues to follow the established three-condition approach. The exemption is determined based on the lowest of prescribed limits, ensuring that only the reasonable portion of HRA remains tax-free.

In simple terms, the exemption is calculated as the least of the following three amounts:

👉 This can be understood clearly through the key components below:

- Actual HRA received from the employer

- Rent paid minus 10% of salary

- 50% of salary (for specified cities) or 40% (for other locations)

This method remains consistent with the earlier framework under the 1962 rules. However, due to changes in city classification and higher rent levels, the practical exemption amount in 2026 may be higher for many salaried employees.

What is ‘Salary’ for HRA Calculation

A correct understanding of “salary” is essential for accurate HRA calculation. Many errors in HRA exemption arise not from the formula, but from using an incorrect salary base.

Under the HRA rules, salary is defined in a limited manner for computation purposes.

👉 The following components are included in salary:

- Basic salary

- Dearness Allowance (if it forms part of retirement benefits)

- Commission (if based on a fixed percentage of turnover)

At the same time, certain components are specifically excluded.

👉 Salary does not include:

- Bonus or incentives

- Allowances such as conveyance or special allowance

- Perquisites

This definition remains aligned with the earlier rules, ensuring continuity in calculation under the income tax rules 2026.

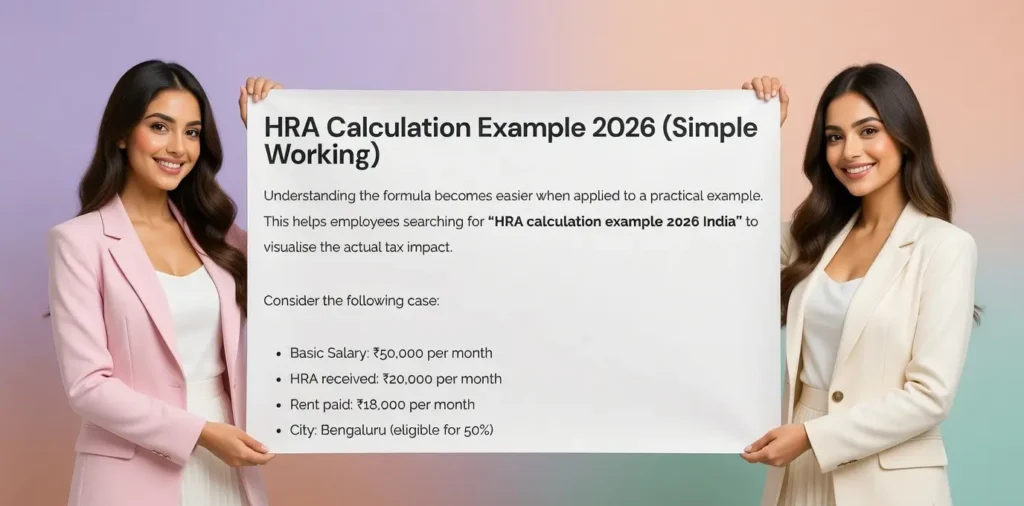

HRA Calculation Example 2026 (Simple Working)

Understanding the formula becomes easier when applied to a practical example. This helps employees searching for “HRA calculation example 2026 India” to visualise the actual tax impact.

Consider the following case:

- Basic Salary: ₹50,000 per month

- HRA received: ₹20,000 per month

- Rent paid: ₹18,000 per month

- City: Bengaluru (eligible for 50%)

Now, applying the formula step-by-step:

👉 The exemption is computed as follows:

- Actual HRA received = ₹2,40,000

- Rent paid – 10% salary = ₹1,56,000

- 50% of salary = ₹3,00,000

👉 The lowest of the above is ₹1,56,000

This amount will be allowed as HRA exemption, and the balance HRA will be taxable.

Impact of 50% Cities on HRA Calculation in 2026

One of the most relevant changes under the income tax rules 2026 is the expansion of cities eligible for the 50% salary threshold. While the formula remains unchanged, this shift directly affects the upper limit of HRA exemption.

For employees evaluating how HRA calculation changes in 2026, the impact is visible in cases where rent is substantial and the higher threshold becomes applicable.

👉 The practical impact can be understood as follows:

- employees in newly included cities may now qualify for higher exemption limits

- a larger portion of HRA may become tax-free, depending on rent levels

- the benefit is more pronounced where rent forms a significant part of salary

This change does not alter the method of calculation, but it enhances the outcome for many salaried employees.

Common Mistakes While Calculating HRA

Errors in HRA calculation are usually not due to complexity, but due to incorrect assumptions or incomplete understanding of the rules.

For employees searching common mistakes in HRA calculation 2026, certain issues appear repeatedly in practice.

👉 The key mistakes include:

- treating the entire HRA received as exempt without applying the formula

- using incorrect salary components for calculation

- claiming HRA without actual payment of rent

- not maintaining proper documentation or rent receipts

- ignoring city classification while applying 40% or 50% rule

Such mistakes can lead to incorrect tax computation and, in some cases, disallowance of exemption. The emphasis under the current framework is on accurate calculation supported by proper records.

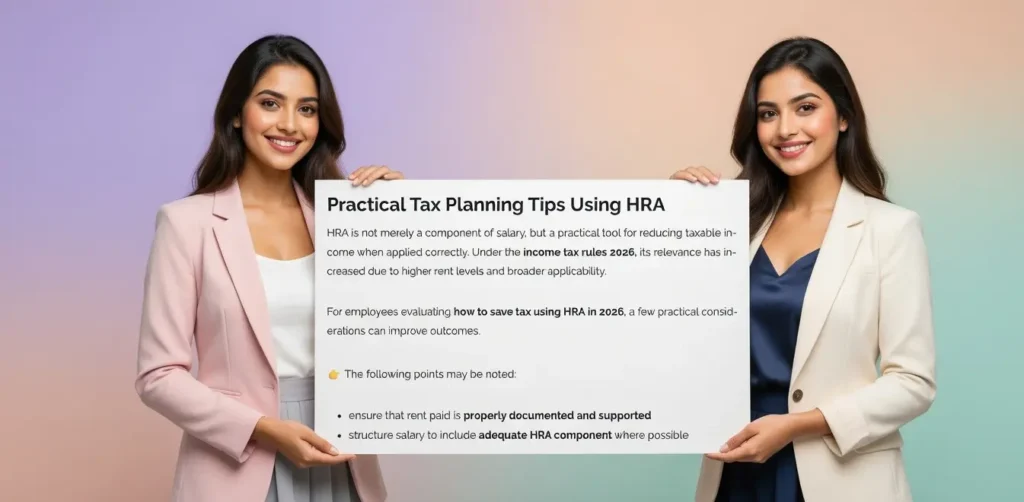

Practical Tax Planning Tips Using HRA

HRA is not merely a component of salary, but a practical tool for reducing taxable income when applied correctly. Under the income tax rules 2026, its relevance has increased due to higher rent levels and broader applicability.

For employees evaluating how to save tax using HRA in 2026, a few practical considerations can improve outcomes.

👉 The following points may be noted:

- ensure that rent paid is properly documented and supported

- structure salary to include adequate HRA component where possible

- consider city classification while evaluating maximum exemption eligibility

- review tax position under old vs new tax regime before claiming HRA

Conclusion

The method of HRA calculation in 2026 continues to follow the established framework, ensuring continuity with earlier rules. However, the expansion of eligible cities and increased emphasis on compliance have enhanced its practical significance.

For salaried employees, the benefit lies not in any change in formula, but in correct calculation, proper documentation and informed application.

FAQs

What is HRA calculation in 2026?

HRA calculation in 2026 is based on the least of three values—actual HRA received, rent paid minus 10% of salary, and 50% or 40% of salary depending on city classification.

Has the HRA calculation formula changed in 2026?

No, the formula remains the same as earlier rules, though the practical impact has changed due to updated city classification and compliance focus.

Which cities qualify for 50% HRA exemption in 2026?

Mumbai, Delhi, Chennai, Kolkata, Hyderabad, Pune, Ahmedabad and Bengaluru fall under the higher exemption category.

Can HRA be claimed under the new tax regime?

No, HRA exemption is not available under the new tax regime.

What is the most common mistake in HRA calculation?

The most common mistake is treating the entire HRA received as tax-free without applying the prescribed calculation method.

Further Reading

For a better understanding of HRA provisions and their practical application, the following related guides may be useful:

- HRA Rules 2026 Explained: Higher Exemption, New Cities & Salary Impact

- Rent Paid to Parents: HRA Rules 2026 and Tax Implications

- Can You Claim HRA Without Paying Rent? Tax Consequences (2026)

- Old vs New Tax Regime 2026: Should Salaried Employees Claim HRA?

Try HRA Calculation Tool

For a quick and accurate estimate, you can use our HRA Calculator for 2026 to check how much exemption you can claim based on your salary, rent and city.

👉 Calculate here: HRA Exemption Calculator AY 2026-27 – Know Taxable HRA Instantly

Sources and References

- Income-tax Act, 1961 — provisions relating to salary income and HRA (Section 10(13A))

- Income Tax Rules, 1962 — earlier framework governing HRA computation (Rule 2A)

- Income Tax Rules, 2026 — restructured rules and updated compliance framework

- Income-tax Act, 2025

- Government notifications and official releases relating to salary taxation and HRA

Disclaimer

This article is intended for general informational purposes based on the applicable provisions relating to HRA rules 2026. The position discussed is of a general nature and may vary depending on individual facts, salary structure and interpretation of rules.

Readers are advised to verify the applicability in their specific case or consult a professional before taking any decision. The law and its interpretation may be subject to further clarification or updates.