Change of Opinion: Why Reassessment Fails

Reassessment fails when based on change of opinion. Learn how courts treat such notices as void despite section 148A and lack of fresh tangible material.

Reassessment fails when based on change of opinion. Learn how courts treat such notices as void despite section 148A and lack of fresh tangible material.

This FAQ section explains the income-tax proposals introduced in Union Budget 2026–27 under the theme of Attracting Global Business and Investment, with specific focus on data centre–related provisions. It covers tax exemptions for foreign companies, conditions applicable to specified data centres, and compliance requirements, helping readers understand the scope and intent of these measures.

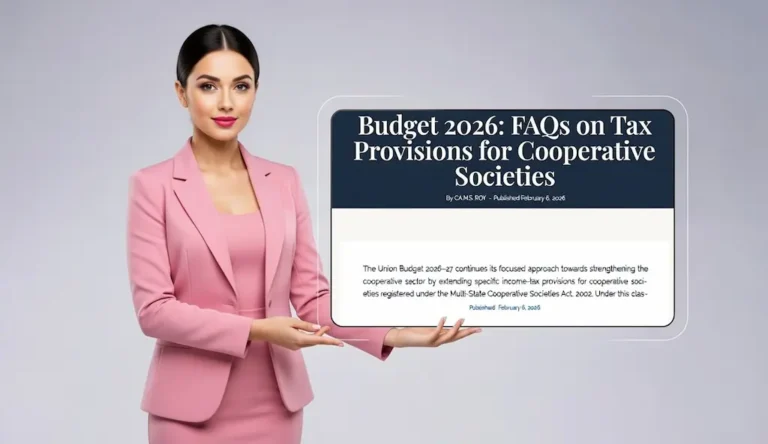

This FAQ section explains the income-tax provisions applicable to cooperative societies under Union Budget 2026–27. It covers key amendments relating to deductions, dividend taxation, federal cooperatives, and inclusion of multi-state cooperative societies under the Income-tax Act, 2025, helping readers clearly understand the scope and applicability of these changes.

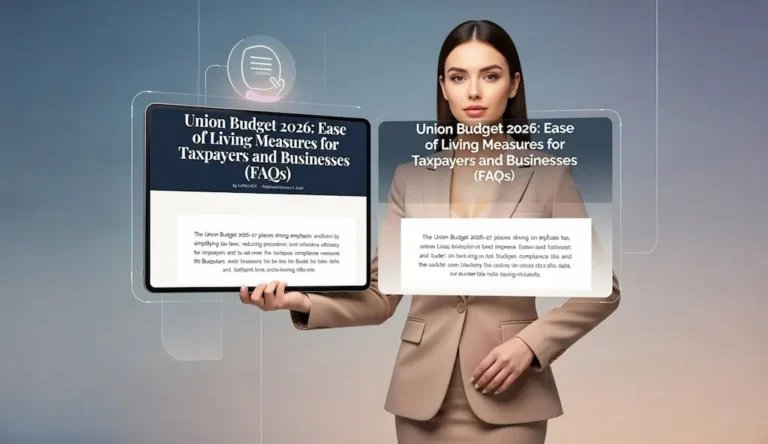

This FAQ section explains the Ease of Living measures introduced in Union Budget 2026, focusing on simplified income-tax compliance, revised return timelines, TDS rationalisation, electronic processes, and taxpayer-friendly reforms under the Income-tax Act, 2025. The FAQs help individuals, professionals, and businesses clearly understand the scope and impact of these changes.

Budget 2026–27 introduces several rationalisation measures across other direct tax provisions. This article reproduces the official FAQs exactly as issued, without interpretation, for professional and exam reference.

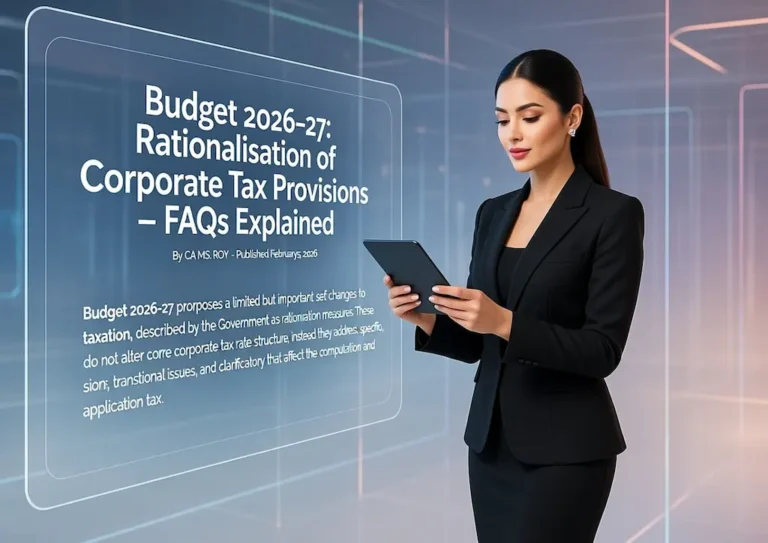

Budget 2026–27 introduces specific rationalisation measures in corporate taxation. This article reproduces all 15 official FAQs exactly as issued, without interpretation.

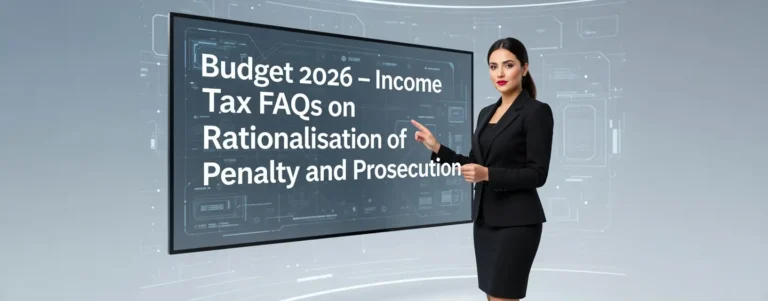

This page compiles official, question-wise FAQs on Income-tax penalties and prosecution provisions as amended by the Finance Bill, 2026, including changes relating to the Income-tax Act, 2025, Updated Returns, Black Money Act, crypto reporting, and search-related assessments.

The Income Tax Department has classified the direct tax proposals of Budget 2026–27 into specific thematic categories to explain the policy intent behind the Finance Bill, 2026. This article explains the official classification of Budget 2026 income tax FAQs, covering ease of living measures, penalty and prosecution reforms, sector-specific initiatives, corporate tax rationalisation, and other direct tax provisions, with links to detailed category-wise FAQ clarifications.

Union Budget 2026 brings important tax changes—from TDS/TCS updates and GST simplification to new Income-tax Act reforms. Here’s what taxpayers must know.

ITC on leasing of commercial property under GST remains available in limited circumstances despite Safari Retreats. This article explains how Section 17(5)(d) applies to lease rentals and construction-linked credits.