Under GST, the supplier usually charges and pays tax. Reverse Charge Mechanism (RCM) flips this in notified cases and makes the recipient pay the tax directly to the Government. This approach improves compliance where collecting tax from many small or hard‑to‑track suppliers would be difficult, and it also covers cross‑border services. If you know when RCM applies, how to pay it, and how to claim input tax credit (ITC), the process becomes routine rather than risky. (source: RCM guide cbec). This guide explains GST Reverse Charge Mechanism (RCM) in simple terms. If you want the nutshell of RCM under GST, jump to the quick summary. We also cover GTA RCM with rates and how to report reverse charge in GSTR-3B step by step.

Quick Summary — Reverse Charge in 60 seconds (2025)

- Who pays? In RCM under GST, the buyer/recipient pays GST instead of the supplier—only for notified goods/services and specific 9(4) cases.

- Typical cases: Individual advocate → business, GTA when not on forward charge, director → company, certain Govt → business services (e.g., renting in specified cases), and import of services.

- 2025 update: From 16-Jan-2025, composition taxpayers are excluded from RCM under GST on the notified renting by unregistered → registered entry; sponsorship by a body corporate moved to forward charge.

- How to pay? Cash ledger only (you can’t use ITC to pay RCM under GST). Then, if eligible, claim ITC in the same period.

- Where to report? GSTR-3B → Liability in Table 3.1(d); ITC in Table 4(A) (domestic RCM in 4(A)(3); import of services in 4(A)(2)). Don’t put RCM inward supplies in GSTR-1.

- Time of supply: Goods → earliest of receipt/payment/30 days from invoice. Services → earlier of payment/60 days from invoice (else book-entry date).

- Docs you need: Supplier invoice must say “tax payable on reverse charge.” For notified 9(4) cases from unregistered suppliers, raise self-invoice + payment voucher.

- Mental model: Pay RCM first → claim ITC (if conditions met) → keep a tidy audit trail.

What is Reverse Charge Mechanism?

RCM under GST is a legal rule that shifts GST liability from the supplier to the recipient for specific categories that the Government has notified. These categories come under Section 9(3) of the CGST Act and Section 5(3) of the IGST Act. Purchases from unregistered suppliers may also attract RCM, but only for notified classes under Section 9(4); the older blanket approach does not apply anymore. In practice, nothing magical happens to the tax itself—the person responsible to pay simply changes.

Example: Why RCM Under GST Matters – A Simple Scenario

ABC Manufacturing Ltd. engages Advocate Mr. Sharma for a ₹50,000 opinion. Because legal services from an individual advocate to a business entity are in the RCM list, Mr. Sharma issues an invoice for ₹50,000 without GST. ABC pays ₹9,000 as GST (18%) in cash while filing GSTR‑3B for that period and, if Section 16 conditions are met, claims ₹9,000 as ITC in the same return cycle. The government gets the same revenue; the compliance duty shifts to ABC, which usually has better systems to pay on time and to document the claim correctly.

Legal Framework and Provisions

The base law is simple: Section 9(3) of the CGST Act allows the Government to notify supplies where the recipient pays tax; Section 9(4) allows RCM on purchases from unregistered persons, but only for notified classes of recipients or supplies. The IGST Act carries mirror provisions at Sections 5(3) and 5(4) for inter‑State and import cases. When RCM under GST applies, the recipient is treated as the person liable to pay tax for that supply, and the usual compliance duties—payment, reporting, and then ITC—follow. (source: CGST Act 2017)

Types of Reverse Charge Scenarios

Type 1 – Nature‑based RCM: The nature of the service or goods itself triggers RCM because it is listed in a notification—for example, legal services to business entities, certain GTA supplies, services by a director to a company, or specified Government services like renting of immovable property. (source: Notification No. 13/2017- Central Tax (Rate)

Type 2 – Registration‑based RCM: Purchases from unregistered suppliers by specific notified classes of registered recipients under Section 9(4). This does not mean every unregistered purchase is under RCM; today, only notified classes/situations are covered.

Goods Subject to Reverse Charge (Illustrative)

Examples include cashew nuts (not shelled/peeled), tendu leaves, tobacco leaves, silk yarn, and supplies by Government bodies such as used vehicles, seized/confiscated goods, old/used goods, and waste & scrap to registered persons. For accuracy, read the current text of Notification 4/2017‑CTR and later amendments such as 36/2017‑CTR, because specific supplier‑recipient combinations matter. (source: Refer Circular No. 76/50/2018-GST)

Services Under Reverse Charge (Key Entries)

Important entries are legal services by an individual advocate or firm to a business entity, GTA services when the GTA has not opted for forward charge, services by a director to the company, certain Government services to business entities (for example, renting of immovable property), insurance agents to insurers, recovery agents to banks/NBFCs, and arbitral tribunals. Always verify the applicable entry in Notification 13/2017‑CTR as amended. (source: refer full list of N/no. 13/2017)

Example: GTA Services – RCM vs Forward Charge

Mumbai Traders Ltd. books transport worth ₹25,000 with a Goods Transport Agency that has not opted for forward charge. In this case, Mumbai Traders pays GST at 5% (₹1,250) under RCM in cash via GSTR‑3B, and, if eligible, takes the same amount as ITC. If the GTA had filed the annual declaration (Annexure V) under Notification 3/2022‑CTR to move to forward charge, the GTA would levy 12% on the invoice and the recipient would not pay RCM on that freight. This single decision by the GTA flips the compliance path for the recipient, so obtain the declaration status at the start of the year and file it for your records.

Recent Changes in 2025 (Read Carefully)

On 16 January 2025, CBIC implemented parts of the 55th GST Council decisions through rate notifications that touched RCM under GST entries. Two practical effects matter to many businesses: first, where sponsorship services are supplied by a body corporate, the liability moved to forward charge; second, composition taxpayers were excluded from RCM for the notified entry relating to renting of commercial/immovable property by an unregistered person to a registered person. The Council also recommended regularizing the period from 10 October 2024 to 15 January 2025. Always check invoice dates and the exact supplier/recipient status before deciding who pays. (source: circular no. 245/02/2025 and GST newsletter)

Example: Impact of 2025 Changes on Businesses

Consider a small restaurant registered under the composition scheme that rents a shop from an unregistered individual. For invoices dated on or after 16 January 2025, that tenant is not covered by the relevant RCM entry, so the tenant does not pay RCM under GST on that rent. If monthly rent is ₹2,00,000, the earlier potential outflow of ₹36,000 (18%) vanishes from the effective date, freeing cash and avoiding extra paperwork. The landlord’s status and the tenant’s scheme matter, so keep a copy of the scheme certificate and note the effective dates on your rent working papers.

Registration Requirements

Any person liable to pay tax under reverse charge must take GST registration even if normal turnover thresholds are not crossed. This enables payment through the electronic cash ledger and the ability to claim ITC where the law permits. (source: CGST-Act)

Time of Supply Under Reverse Charges

Time of supply sets the ‘when’ of your tax liability. For goods, pick the earliest of the date you receive the goods, the date of payment, or the day immediately after 30 days from the supplier’s invoice; if none can be identified, use the date the entry hits your books. For services, pick the earlier of the payment date or the day immediately after 60 days from the supplier’s invoice; if that still cannot be determined, fall back to the books entry date. Getting this right prevents interest from building silently in the background. (source: Sec 13 of CGST)

Example: Time of Supply – Services under RCM

A consulting invoice dated 5 April reaches your office, but payment drags. If you still have not paid by 4 June—sixty days later—the time of supply clicks to 5 June and interest may apply from that date if the tax has not been discharged. If you had paid, say, on 10 May, that payment date would have been your time of supply, and the interest meter would never start. A simple reminder inside the accounts team to check 30‑/60‑day limits each week avoids surprises.

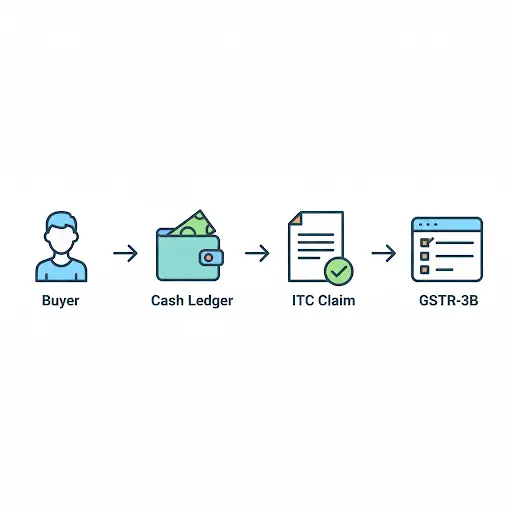

GST Liability & ITC on Reverse Charges

Discharge RCM using the electronic cash ledger while filing GSTR‑3B; you cannot use ITC to pay RCM. Once paid, and if Section 16 conditions are satisfied—valid document, receipt of goods/services, tax actually paid, and return filed—you may claim ITC in the same period. Show the liability in Table 3.1(d) and claim ITC in Table 4(A), typically 4(A)(3) for domestic RCM and 4(A)(2) for import of services. (source: FAQ GSTR 3B)

Invoicing & Documentation for Reverse Charges

The supplier’s invoice must state whether tax is payable on reverse charge, as per Rule 46(p). When you procure from an unregistered supplier in a notified 9(4) situation, you must issue a self‑invoice under Section 31(3)(f) and a payment voucher under Section 31(3)(g) read with Rule 52. File these with your RCM workings, bank challans, and GSTR‑3B extracts; auditors love tidy trails, and so does the portal if you ever need to reconcile.

Payment and Compliance Requirements

Pay RCM strictly via cash ledger, keep proofs, and line up your internal approvals a few days before the GSTR‑3B due date. If you work on the QRMP scheme, align cash flows so that RCM outgo in the quarter does not surprise you at filing time. Where possible, settle vendor terms to avoid crossing the 30‑/60‑day clocks for time of supply. (source: FAQ GSTR3B)

Common Compliance Pitfalls (What to Avoid)

Treating every unregistered purchase as RCM without checking Section 9(4) notifications; trying to pay RCM with ITC; forgetting to issue a self‑invoice or payment voucher; or reporting RCM in GSTR‑1 instead of GSTR‑3B. Another frequent miss is failing to obtain the GTA’s forward‑charge declaration at the start of the year, which leads to wrong treatment all year. (source: Notification13/2017-CGST)

Practical Compliance Checklist

1) Identify the notification entry for your goods/services. 2) Capture supplier status (registered/unregistered; GTA forward/RCM). 3) For notified 9(4) cases, issue self‑invoice and payment voucher. 4) Pay via cash ledger in GSTR‑3B Table 3.1(d). 5) Claim eligible ITC in Table 4(A). 6) Track time‑of‑supply limits (30 days for goods, 60 for services). 7) Maintain a monthly RCM file with invoices, challans, and ledger proofs.

Case-laws

1) Union of India v. Mohit Minerals Pvt. Ltd. (Supreme Court, 19-May-2022) — Matter: Validity of IGST under RCM on ocean freight for CIF imports via notifications. Judgment: The Supreme Court set aside the levy—IGST is already charged on the CIF value at customs; a separate RCM levy on ocean freight would cause impermissible double taxation, and in CIF contracts the importer isn’t the “recipient” of the freight service. Takeaway: No RCM on ocean freight in CIF imports; review past demands/refunds per limitation. (Source: SCI API)

2) M/s Anjani Cotton Industries v. Principal Commissioner of CGST & Anr. (Gujarat High Court, 03-May-2024) — Matter: RCM on raw cotton purchased from agriculturists; pleas on Sections 9(3)/9(4), revenue-neutrality (exports) and limitation. Judgment: The High Court upheld RCM under Section 9(3) read with the notified entry for raw cotton, sustaining demand (and equal penalty) on facts; “revenue-neutrality” wasn’t accepted as a defence. Takeaway: Registered buyers of raw cotton from agriculturists must discharge RCM per the notified entry with tight documentation and timely cash payment. (Official record of SLP against this HC judgment is on the Supreme Court site- SCI API)

Technology Tips

Use simple ERP rules: tag RCM vendors, lock payment mode to cash ledger for such bills, auto‑generate self‑invoices and payment vouchers, and run a month‑end exception report that flags any expense GL booked without RCM logic. Even a spreadsheet tracker with filters on vendor type and due‑date counters can reduce errors dramatically.

Conclusion

RCM is predictable once you follow the same steps every time: check the notification, decide who pays, discharge the tax in cash through GSTR‑3B, and then claim eligible ITC. Keep documents tidy, note the 2025 updates for sponsorship and renting, and use reminders so the 30‑/60‑day clocks never surprise you.

FAQ on RCM Under GST

Q. Do I always pay RCM when I buy from an unregistered person?

A. No. Section 9(4) now applies only to notified classes/situations. Check the latest notification before treating such purchases as RCM.

Q. Where do I report RCM in returns?

A. Report liability in GSTR‑3B Table 3.1(d) and claim eligible ITC in Table 4(A). Do not show these inward supplies in GSTR‑1.

Q. Can I claim ITC of RCM in the same month?

A. Yes, provided Section 16 conditions are met. Remember that the RCM payment itself must be made in cash.

Q. When is RCM applicable on GTA?

A. RCM applies when the GTA has not opted for forward charge; if the GTA opts via Annexure V (Notification 3/2022‑CTR), the GTA charges 12% and RCM does not apply for that supply.

Q. What changed in January 2025 for renting and sponsorship?

A. Composition taxpayers were excluded from RCM for the notified renting entry, and sponsorship by a body corporate moved to forward charge per 55th Council decisions notified on 16 January 2025

Q6. Does RCM apply on import of goods?

A. No. IGST on import of goods is paid at customs on the Bill of Entry (not through GSTR-3B 3.1(d)). You may claim ITC from that Bill of Entry. RCM in GSTR-3B applies to import of services, not goods.

Q7. Are advances under RCM taxable?

A. For services, yes—paying an advance can trigger time of supply (earlier of payment date or 60 days from invoice). For goods under RCM, the time of supply is the earliest of receipt of goods, payment date, or 30 days from the supplier invoice—so an advance can also trigger liability. Keep dates tight to avoid interest.

Q8. If I pay RCM, do I always get ITC?

A. You can take ITC only if the supply is used for business, not hit by blocked-credit rules (Section 17(5)), and you meet basics: valid document (or self-invoice/payment voucher where required), tax actually paid, and returns filed. If it’s a blocked category (e.g., certain motor vehicles), ITC won’t be allowed even though you paid RCM.

Q9. I missed RCM earlier—what now?

A. Pay the tax with interest (Section 50) immediately, then claim ITC in the current return if still within the Section 16(4) time limit for that financial year. Keep a small working paper showing the original invoice date, when you paid, and where you claimed ITC.

Q10. Do I need GST registration if my only liability is under RCM?

A. Yes. Persons liable to pay tax under reverse charge must register compulsorily (even if turnover is below threshold). Registration lets you discharge RCM and, where eligible, claim ITC.

Disclaimer

This article is for general information only and is based on Indian GST law and guidance as of September 2025. It is not professional advice or a legal opinion, and reading it does not create a CA–client relationship with TaxBizMantra or the author. GST provisions, notifications, and judicial positions change over time and their application depends on your specific facts. Examples are illustrative; your eligibility for ITC, rate, place/time of supply, and reporting may differ. Always verify with official sources and consult your professional advisor before acting. While we strive for accuracy, no warranty is given and no liability is accepted for any loss arising from reliance on this content. External links are provided for convenience—we are not responsible for their content or updates. Case-law notes are summaries; check the full judgments and any subsequent orders/appeals before relying on them.

Further reading

GST Registration – Checklist & Documents

Key Official Sources & References

Notification 13/2017-CTR (Services under RCM) –Read now

Notification 4/2017-CTR (Goods under RCM) – GST Council page: Read now

Clarification referencing 36/2017-CTR (Govt supplies of used vehicles, scrap): Read now

Notification 3/2022-CTR (GTA forward-charge option, Annexure V): Read Now

55th GST Council services circular / update (covers 07/2025-CTR effects): Read now

GST Council newsletter (Jan 2025) – composition exclusion note: Read now

GSTR‑3B Help – where to report RCM (Table 3.1(d), 4(A)): Read now

CGST Act (Sections 9, 12, 13, 31) – CBIC consolidated PDF: Read now

GST Council flyer – Tax invoice & other documents (Rule 46 mention): Read now

Rule 52 (payment voucher) – CBIC Tax Information: Read now

Note: This guide is based on provisions as of January 2025. Readers should verify current notifications and amendments for latest compliance requirements