HRA without paying rent is a common question among salaried employees, especially when House Rent Allowance forms part of their salary. However, a persistent misconception continues to create risk — can HRA be claimed even when no rent is actually paid?

House Rent Allowance (HRA) remains one of the most commonly claimed tax exemptions by salaried employees. In practice, many taxpayers assume that the presence of HRA in salary and its reflection in Form 16 automatically entitles them to exemption. This assumption, while widespread, does not align with the statutory framework and can lead to unintended tax exposure if HRA is claimed without paying rent.

With the increasing use of data-backed scrutiny, AIS integration, and PAN-linked verification, tax authorities now have enhanced capability to identify inconsistencies between claimed exemptions and actual financial behaviour. What may appear as a routine claim at the time of filing can subsequently result in disallowance, additional tax liability, and exposure to interest and penalties.

This is not merely a technical issue — it is a compliance risk that is increasingly being examined in assessments.

This article is based on the provisions of the Income-tax Act, 2025 effective from 1 April 2026 (FY 2026–27 / AY 2027–28) and applicable rules.

It addresses one specific question:

What happens if HRA is claimed without paying rent?

Why People Claim HRA Without Paying Rent

Claiming HRA without paying rent is less about interpretation of law and more about perception of compliance.

A common scenario is where employees continue to receive HRA as part of their salary while living in their own house or with family. Since the allowance is already factored into payroll, there is a natural tendency to assume that the exemption is equally available.

Verification at the employer level is primarily based on declarations and may not involve detailed examination of underlying transactions. This often creates a misplaced sense of comfort.

However, exemption under HRA is governed by statutory conditions that operate independently of payroll processing.

Informal advice further reinforces this behaviour — the belief that such claims are routine and rarely questioned. However, this overlooks a fundamental distinction:

Receipt of HRA is not the same as eligibility for exemption.

It is this gap between perceived compliance and statutory eligibility where the real risk begins.

What Happens If You Claim HRA Without Paying Rent

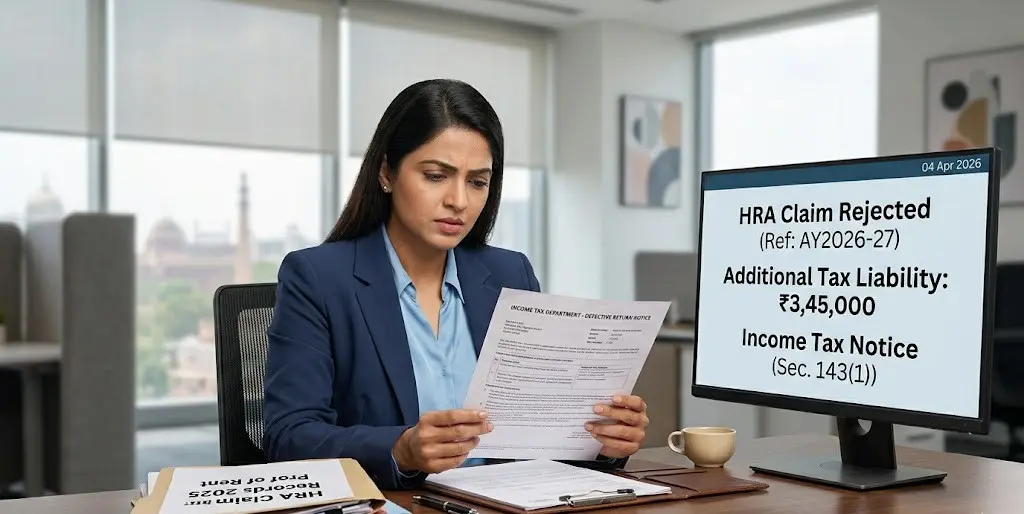

The consequence of claiming HRA without paying rent does not arise at the time of filing itself, but typically during verification or assessment.

HRA exemption is inherently linked to actual expenditure on rent. Where no such expenditure exists, the claim lacks factual support. In such cases, the exemption claimed may be liable to be disallowed upon examination.

The practical implication is:

The exemption claimed is withdrawn

Total income is recomputed

Additional tax becomes payable

This adjustment may arise through automated checks, verification processes, or scrutiny proceedings. Importantly, the responsibility to substantiate the claim rests entirely with the taxpayer.

An HRA claim without supporting evidence is unlikely to sustain under verification.

What may appear acceptable at the return filing stage can therefore translate into tax exposure at a later stage, once examined against actual financial records.

How Such Claims Get Detected

The detection of incorrect HRA claims has become more structured with the use of data analytics and cross-verification mechanisms.

Salary details, including HRA components, are already available with the tax authorities through employer reporting. When an exemption is claimed without adequate supporting evidence or a corresponding financial trail, it may give rise to inconsistencies requiring further verification.

While direct reporting of rent payments may not always be available, patterns such as disproportionate exemption claims or absence of supporting indicators can trigger review.

Certain situations are more likely to attract attention:

Repeated HRA claims without demonstrable rent outflow

High exemption amounts without corresponding financial activity

Inconsistent or unverifiable supporting details

These factors do not automatically result in adverse action, but they increase the likelihood of further enquiry, notice, or scrutiny selection.

In the current framework, detection is increasingly driven by data consistency rather than isolated verification.

What Happens After Detection

Once an HRA claim without actual rent payment is flagged, the matter typically proceeds to verification or assessment.

The taxpayer may be required to provide supporting evidence to substantiate the exemption claimed. In the absence of actual rent payment, such substantiation becomes difficult.

If the explanation is not satisfactory, the assessing authority may:

Disallow the HRA exemption claimed

Recompute total income

Raise a tax demand for the differential amount

Depending on the nature of the case, this may be concluded through summary adjustments or detailed scrutiny proceedings. However, the outcome remains consistent — the exemption does not survive without factual support.

A claimed tax benefit, once examined, must be supported by actual transactions.

Tax Impact and Financial Consequences of HRA without paying rent

The financial impact of an incorrect HRA claim extends beyond the reversal of exemption.

The immediate effect is an increase in taxable income, resulting in additional tax payable as per applicable slab rates if HRA is claimed without paying rent.

In addition, the following consequences may arise:

Interest liability on the shortfall in tax paid

Recalculation of total tax dues for the relevant year

In certain cases, depending on the facts and explanations provided, the matter may also attract penalty implications under provisions relating to under-reporting or misreporting of income.

The cumulative effect can be significant — a relatively small exemption, when disallowed, may lead to a higher overall outflow due to tax and interest, and potentially penalty.

The financial impact of non-compliance often exceeds the perceived benefit of the claim.

Living With Parents Without Rent — Why the Claim Fails

A commonly misunderstood situation arises where employees Living With Parents Without Rent assume that HRA exemption can still be claimed, even in the absence of actual rent payment.

From a tax perspective, the relationship between the parties is not the determining factor. What matters is the existence of a genuine rental arrangement supported by actual financial outflow.

Where no rent is paid, the arrangement lacks the fundamental element required for exemption. The mere fact of residing in a parental home does not create eligibility.

Even in cases where a notional or informal understanding exists, without corresponding evidence of payment, the claim does not withstand verification. In fact, such cases often attract closer examination due to the ease with which non-genuine arrangements can be structured.

It is important to distinguish between:

Living with parents without rent) → No exemption

Paying rent to parents (genuine transaction) → May be considered, subject to proper documentation and tax reporting

The exemption is linked to the transaction, not the relationship.

Where the transaction itself is absent, the claim does not meet the basic threshold for allowance.

Final Verdict — Is It Ever Worth the Risk?

The position under the applicable law is clear:

HRA exemption is not available in the absence of actual rent payment.

What may appear as a routine claim at the time of filing can subsequently result in tax exposure upon verification.

The consequences are not limited to disallowance. The combined impact of additional tax, interest, and potential penalty can outweigh any short-term benefit.

From a compliance perspective, this is not a grey area but a basic eligibility condition.

Tax planning is effective only when it is capable of withstanding verification.

FAQs — HRA Without Paying Rent (2026)

Can HRA be claimed if no rent is paid?

No. HRA exemption is linked to actual rent expenditure. In the absence of rent payment, the exemption is not allowable.

What happens if HRA is claimed incorrectly?

The exemption may be disallowed during verification or assessment. The amount is added back to income, resulting in additional tax liability along with applicable interest.

Will every incorrect HRA claim be detected?

Not necessarily in every case, but with increasing data integration and reporting, the likelihood of detection has significantly increased.

Can HRA be claimed while living with parents without rent payment?

No. Simply residing with parents does not qualify for exemption unless there is a genuine rent arrangement supported by actual payment.

Is there any partial exemption available of HRA without paying rent?

No. Without rent payment, the exemption mechanism does not apply, and the claim is not valid.

Does employer approval make the claim valid?

No. Employer processing or inclusion in Form 16 does not determine final tax eligibility. The claim must satisfy legal conditions at the time of filing and verification.

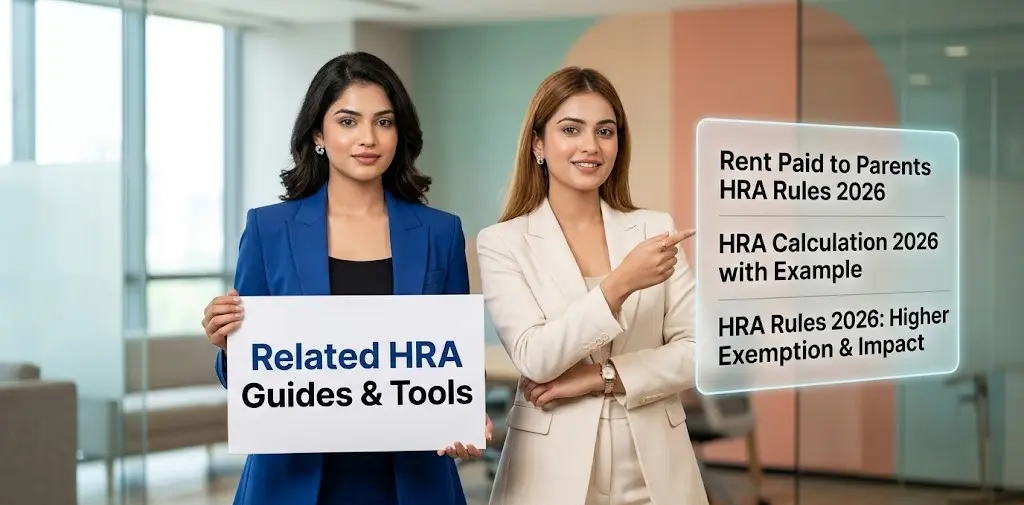

Related HRA Guides & Tools

To better understand HRA rules and avoid incorrect claims, you may also explore these detailed guides:

Learn how HRA exemption is calculated step-by-step with real examples, including salary components, metro vs non-metro treatment, and practical scenarios.

The information provided in this article is for general informational and educational purposes only and does not constitute professional advice. While every effort has been made to ensure accuracy, readers are advised to verify the applicability of provisions based on their specific facts and consult a qualified professional before taking any action.

This article is based on the provisions of the Income-tax Act, 2025 effective from 1 April 2026 (Financial Year 2026–27 / Assessment Year 2027–28) and applicable rules. Tax laws are subject to amendments, notifications, and judicial interpretations, and the applicability of provisions may vary.

The author and publisher shall not be liable for any loss or consequences arising from reliance on the information contained in this article.

CA M.S. Roy is a Chartered Accountant with 13+ years of experience in taxation, financial reporting, Ind AS implementation, consolidation, and complex accounting matters. He has led carve-outs, common control business combinations, and large-scale financial transformations across manufacturing and infrastructure sectors. Through TaxBizMantra, he simplifies tax and finance concepts for professionals and businesses using practical, standards-driven insights.

Income Tax Slabs AY 2026-27 (FY 2025-26) Every April, the math changes on how much of your income you actually keep. For AY 2026–27 (FY 2025–26), the Union Budget 2025 reshaped the New Tax Regime with a wider 7‑slab structure and relief designed so that no…

The Income Tax Department has classified the direct tax proposals of Budget 2026–27 into specific thematic categories to explain the policy intent behind the Finance Bill, 2026. This article explains the official classification of Budget 2026 income tax FAQs, covering ease of living measures, penalty and prosecution reforms, sector-specific initiatives, corporate tax rationalisation, and other direct tax provisions, with links to detailed category-wise FAQ clarifications.

This FAQ section explains the Ease of Living measures introduced in Union Budget 2026, focusing on simplified income-tax compliance, revised return timelines, TDS rationalisation, electronic processes, and taxpayer-friendly reforms under the Income-tax Act, 2025. The FAQs help individuals, professionals, and businesses clearly understand the scope and impact of these changes.

Learn everything about the Intimation notice u/s 143(1) of Income Tax — its meaning, key reasons for issuance, how to respond, and the time limit for rectification under the 2025 Income Tax guidelines.

Form 168 income tax reporting is emerging as part of India’s evolving tax compliance framework under the new Income-tax Act, 2025. Understand how Form 168 differs from Form 26AS, its connection with AIS and TIS, and what taxpayers should verify before filing ITR for AY 2026-27.

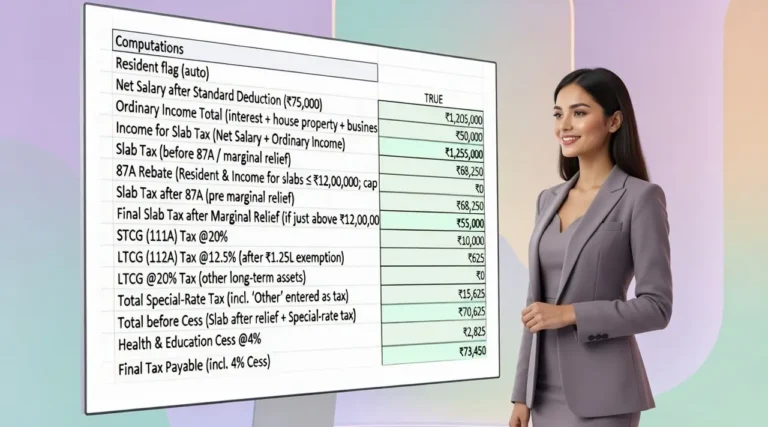

Download our free Excel Income Tax Calculator for AY 2026–27 (FY 2025–26). Built with the latest New Regime slab rates, ₹75,000 standard deduction, Section 87A rebate, and capital gains tax updates, this easy-to-use tool lets you compute your tax in minutes. Perfect for salaried, pensioners, and NRIs to plan taxes quickly and accurately.