How to Exit NPS in the New Tax Regime —

PFRDA’s 2025 Rules, the ₹5 Lakh Threshold & Your Smartest Options

PFRDA’s December 2025 exit rules changed everything. If you opened an NPS account for the 80C tax benefit — and now want out — here is the complete guide to NPS withdrawal under the new tax regime: who can exit freely, who is trapped, and three strategies better than a premature closure.

Quick Answer — How to Exit NPS in the New Tax Regime

Corpus ≤ ₹5 lakh: Apply for voluntary exit on the CRA portal — receive 100% as lump sum. | Corpus > ₹5 lakh: Do not rush. Voluntary exit locks 80% in an annuity forever. Use Section 80CCD(2), wait for normal exit, or optimise NPS as a low-cost retirement bucket instead.

If you are searching for how to exit NPS in the new tax regime, you are not alone. Millions of salaried Indians opened a National Pension System (NPS) account for one reason: the extra ₹50,000 deduction under Section 80CCD(1B), stacked on top of the ₹1.5 lakh Section 80C limit. Together, these allowed a total NPS tax benefit of up to ₹2 lakh under the old tax regime — a compelling, clean deal.

Then the new tax regime arrived as the default for most employees, stripping out both Section 80C and Section 80CCD(1B). The NPS tax benefit that made the account attractive is gone. What remains — the account, the corpus, and the exit rules — is what you now need to navigate carefully.

Good news: PFRDA’s Exits and Withdrawals (Amendment) Regulations, notified on December 12, 2025, made NPS voluntary exit significantly more accessible. But the rules are not uniform — they pivot sharply at one number. Here is everything you need to know.

PFRDA Exit Rules 2025: Three Changes That Matter

The PFRDA Exits and Withdrawals (Amendment) Regulations 2025 introduced three key changes for non-government subscribers — both All Citizen Model and Corporate NPS subscribers.

Five-year lock-in abolished. Non-government NPS subscribers can now apply for voluntary exit at any point — no minimum subscription period required.

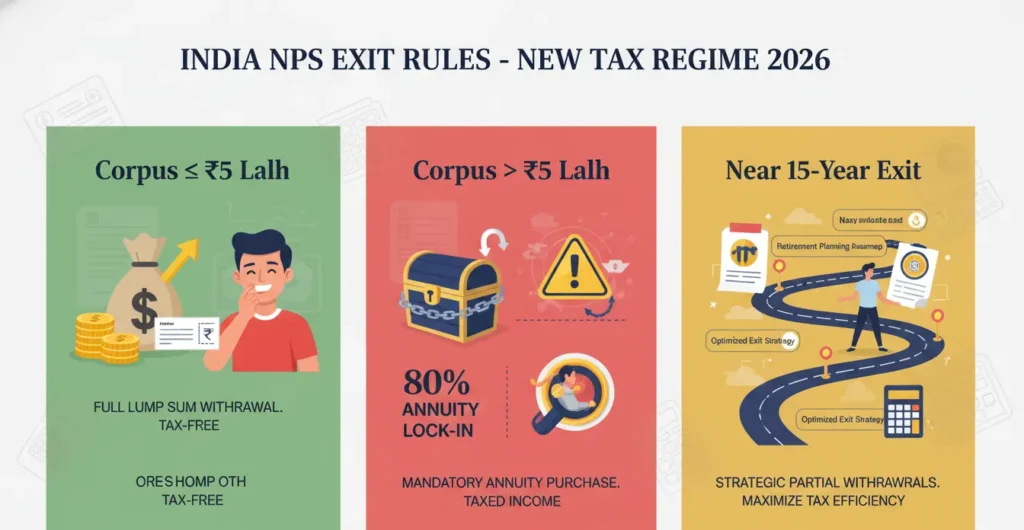

Small-account threshold doubled to ₹5 lakh. If your total accumulated pension wealth (corpus) is ₹5 lakh or below, a voluntary exit entitles you to 100% of the corpus as a lump sum. The earlier threshold was ₹2.5 lakh.

Above ₹5 lakh, the 80% annuity rule applies on voluntary exit. For corpora exceeding ₹5 lakh, a voluntary NPS premature withdrawal requires 80% of the corpus to fund a compulsory annuity. Only 20% is paid as lump sum.

Your first step: log in to the CRA portal at cra.nps-proteantech.in (formerly cra-nsdl.com) using your PRAN (Permanent Retirement Account Number), check your corpus, and determine which side of the ₹5 lakh line you fall on. That single number determines your entire strategy.

Scenario A: How to Close Your NPS Account When Corpus is Below ₹5 Lakh

Most accounts opened purely for the ₹50,000 annual deduction — especially those started in 2022 or later, or those with inconsistent contributions — will likely have accumulated a corpus under ₹5 lakh. At ₹50,000 per year for three to four years, with moderate equity returns, balances often sit well within this threshold.

File a voluntary exit request on the CRA portal. Verify your linked bank account. Under PFRDA’s 2025 rules, you receive 100% of your NPS corpus as a lump sum, typically credited within 5–10 working days.

Under Section 10(12A) of the Income Tax Act, 60% of any NPS lump sum at exit is fully tax-exempt. The remaining 40% is added to your taxable income for the year. For corpora under ₹2–3 lakh, the basic exemption limit or rebate under the new regime absorbs most or all of the taxable portion.

One procedural note for those who were in Corporate NPS and have since left their employer: file Form ISS-1 to shift your PRAN from the Corporate Model to the All Citizen Model. Your corpus and PRAN number stay unchanged — this is an administrative reclassification only.

Scenario B: NPS Premature Withdrawal When Corpus Exceeds ₹5 Lakh — The Annuity Trap

This is where most people make a costly, irreversible mistake. Understanding NPS annuity rules India is critical before you act.

On a ₹7 lakh corpus, voluntary NPS exit gives you just ₹1.4 lakh in hand. The remaining ₹5.6 lakh is locked irrevocably into a life annuity — a monthly pension you cannot reverse, surrender, or reinvest at a later date.

Current annuity rates from PFRDA-empanelled life insurers in India range between 4% and 6.5% per year. A subscriber aged 35–40 will typically receive rates in the lower range because the insurer prices in decades of payouts. At 5% on ₹5.6 lakh, your monthly annuity income would be roughly ₹2,333 — fully taxable at your slab rate, illiquid, and fixed regardless of inflation or market returns.

Three Smart Paths for NPS Subscribers Above ₹5 Lakh

Path 1 — Wait for Normal NPS Exit (15-Year Rule)

Normal exit — as distinct from voluntary exit — now triggers at two points: 15 years of subscription, or reaching age 60, whichever comes first. At normal exit, the rules are considerably more generous than for voluntary NPS premature withdrawal. Corpora up to ₹8 lakh at normal exit can be received fully as a lump sum, bypassing the annuity requirement entirely.

If you opened your NPS account in 2010 or 2011, you may already be approaching or at the 15-year mark. The minimum annual contribution to keep an All Citizen NPS account active is just ₹1,000. Contribute the minimum, wait for normal exit eligibility, and walk away with your entire corpus intact.

₹1,000 per year. That is all you need to prevent account freeze while you wait out the remaining years to normal exit. Do not contribute more than necessary if you simply want to preserve the account.

Path 2 — Convert NPS into a Low-Cost Retirement Engine

NPS has one advantage that the new tax regime cannot remove: it is the lowest-cost pension vehicle available to Indian retail investors. Pension funds under the Common Scheme charge a maximum of 0.12% per year in fund management fees. Even under the Multiple Scheme Framework (MSF), the cap is 0.30%. Compare this with equity mutual funds at 1%–1.5% in direct plans — the compounding cost advantage over 15–20 years is significant.

PFRDA now also permits up to 100% equity allocation under Scheme E within NPS. If you are in your 30s or 40s with a corpus trapped above ₹5 lakh, shifting to a high-equity pension fund and letting it compound at ultra-low cost until normal exit may be the most rational available path — far better than the permanent annuity lock-in from voluntary exit.

Path 3 — Use Section 80CCD(2): The Only NPS Tax Benefit That Survived the New Tax Regime

This is the single most actionable strategy for salaried individuals. Section 80CCD(2) is fully available under the new tax regime — and it is more generous than before.

Under Section 80CCD(2), employer contributions to your NPS Tier I account are deductible from your taxable salary — up to 14% of Basic Salary plus Dearness Allowance for all employees (raised from 10% for private sector employees, effective FY 2024–25). This employer NPS contribution is deductible over and above the standard deduction and any other limits — it does not count towards the ₹1.5 lakh Section 80C ceiling.

Note: The combined employer contributions to EPF, NPS, and superannuation fund are tax-free only up to a total of ₹7.5 lakh per year. Amounts above this are taxable in your hands.

Ask your HR or payroll department whether your employer is registered under Corporate NPS and whether a portion of your CTC can be restructured as an employer NPS contribution under Section 80CCD(2). For a 30% slab taxpayer with a ₹10 lakh basic salary, this alone can save ₹42,000+ in annual tax — and the money goes into your own NPS account, not lost.

NPS Exit Decision Table — What to Do Based on Your Situation

| Your Situation | Recommended Action | Key Reason |

|---|---|---|

| Corpus ≤ ₹5 lakh, no interest in NPS | File voluntary NPS exit on CRA portal | 100% lump sum under PFRDA 2025 rules; low tax impact |

| Corpus > ₹5 lakh, want immediate exit | Pause — exhaust all alternatives first | Voluntary exit locks 80% in an irreversible annuity |

| Account opened before 2012, near 15 years | Pay ₹1,000/year minimum, wait for normal exit | Normal exit allows corpus up to ₹8 lakh without annuity |

| Salaried, employer has Corporate NPS | Use Section 80CCD(2) — route CTC as employer NPS | Only surviving NPS deduction in new tax regime; saves 20–30% tax |

| 10+ years to retirement, growing corpus | Shift to 100% Scheme E within NPS | Ultra-low fees (0.12%–0.30%) + equity compounding |

| Self-employed, switched to new tax regime | No mandatory exit — maintain ₹1,000/year minimum | 80CCD(2) not available; keep corpus growing at low cost |

The Real Question Isn’t “How Do I Get Out?” — It’s “What’s My Best Move?”

The reason so many people feel stuck in NPS today is that they entered for the wrong reason — a tax deduction — and now, without that deduction under the new tax regime, the account feels like a liability. But the account itself is not the problem; the urgency to exit without thinking is.

If your NPS corpus is below ₹5 lakh, exit cleanly, redeploy the funds into PPF, mutual funds, or any instrument better suited to your goals, and move on. If your corpus exceeds ₹5 lakh, do not let impatience drive a permanent decision. The 80% annuity trap under NPS voluntary exit rules is irreversible. Patience, minimum contributions, and a disciplined wait for normal exit will leave you in a far stronger financial position.

For salaried individuals still in the accumulation phase: the NPS conversation is no longer about Section 80C. It is about Section 80CCD(2), ultra-low costs, and long-horizon compounding. Reframed correctly, NPS still makes sense — just for different reasons than it did five years ago.

Frequently Asked Questions — NPS Exit & New Tax Regime

Related Resources

Explore these related tools, calculators, and in-depth guides to better understand the new tax regime, NPS withdrawal rules, retirement planning strategies, and the tax-saving opportunities still available under Section 80CCD(2). These resources will help you make smarter long-term financial and pension decisions before exiting your NPS account.

Related Posts

- New Tax Regime vs Old Tax Regime: Which Is Better in 2026?

- Section 80CCD(2) Explained: The Last Major NPS Tax Benefit in New Regime

- NPS vs PPF: Which Is Better for Retirement Planning?

- NPS Taxability Explained: Withdrawal, Maturity & Annuity Rules

- How Employer NPS Contribution Reduces Tax Under New Regime

- Best Retirement Planning Options After the New Tax Regime

- Rent Or Buy House In India? What The Math Says + Calculator

Related Tools

- New Tax Regime vs Old Tax Regime Calculator

- Income Tax Calculator FY 2025-26

- NPS Tax Benefit Calculator

- Retirement Corpus Calculator

- SIP Calculator

- Salary Structure Optimizer (Section 80CCD(2))

- EPF vs NPS Comparison Tool

- Gratuity Calculator

Disclaimer: This article is for general informational purposes only and does not constitute investment or tax advice. Tax laws and PFRDA regulations are subject to change. Readers should consult a qualified chartered accountant or SEBI-registered financial adviser before making decisions about their NPS account. All facts reflect PFRDA regulations and Income Tax Act provisions as of May 2026.