The June 2026 Ordinance Changed the Rules—But Not the Debate

The June 2026 G-Sec ordinance is a welcome first step — but a piecemeal exemption is not a strategy. India needs to go further, and the new Income Tax Act, 2025 gives it the legal architecture to do exactly that.

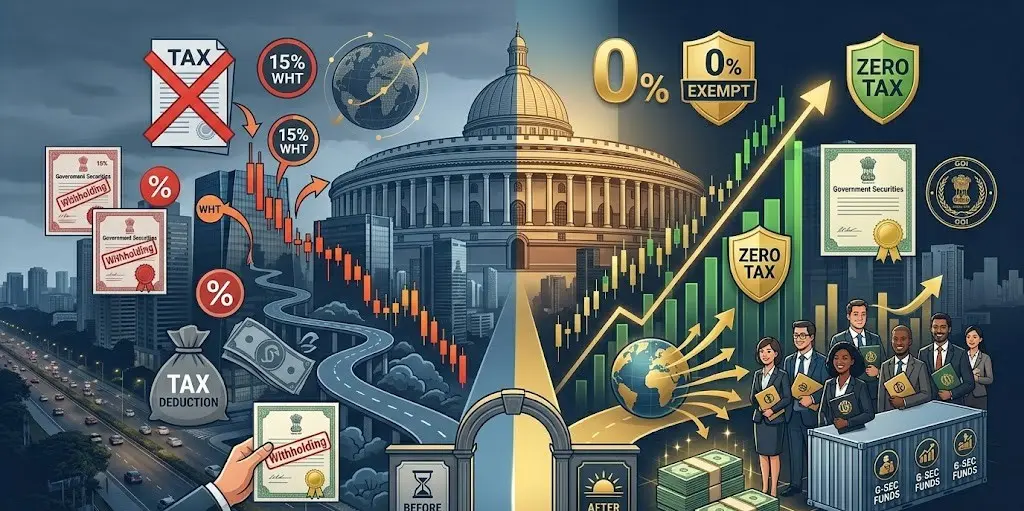

Capital gains tax on foreign investors in India has returned to the centre of policy debate following the promulgation of the Income-Tax (Amendment) Ordinance, 2026 on 5 June 2026. The Ordinance exempts Foreign Institutional Investors (FIIs) from tax on both capital gains and interest income arising from Government Securities with retrospective effect from 1 April 2026. It was a striking move: an emergency presidential ordinance issued under Article 123 because Parliament was not in session. The message to global bond markets was unmistakable. The question now is whether that message goes far enough.

India is the world’s most populous country, one of its fastest-growing major economies, and has spent the better part of a decade marketing itself as the world’s preferred destination for mobile capital. Yet for most foreign investors, navigating India’s capital gains tax architecture has remained a lesson in friction, ambiguity, and structural deterrence. The June 2026 ordinance is a beginning. This editorial argues it should be a catalyst for something bolder: a comprehensive, structured abolition — or at minimum, near-zero taxation — of capital gains for qualifying foreign investors across all major asset classes.

What the June 2026 Ordinance Actually Does — and What It Doesn’t

The Income-Tax (Amendment) Ordinance, 2026 (Ordinance No. 2 of 2026) amends Schedule IV of the Income-Tax Act, 2025 by inserting two new exemption entries. Entry 13D covers Foreign Institutional Investors (FIIs) as defined under S.210(6)(a), IT Act 2025 [cf. old S.115AD(1), IT Act 1961]. Entry 13E covers the Bank for International Settlements (BIS). Both entries grant a full income-tax exemption on interest income and capital gains on “Government securities” — a term defined by reference to S.2(f), Government Securities Act, 2006, thus covering central government dated securities, Treasury Bills, and all other sovereign debt instruments issued under that Act.

Before (pre-1 April 2026): FIIs paid 12.5% LTCG on listed bonds held over 12 months under S.210, IT Act 2025 [old S.115AD], plus withholding tax at applicable rates on interest from G-Secs. Under the Fully Accessible Route (FAR) introduced by RBI, a concessional TDS rate of 5% on G-Sec interest had applied under old S.194LD of the IT Act 1961.

After (w.e.f. 1 April 2026): Full exemption on both interest income and capital gains on Government securities for FIIs (Entry 13D) and the BIS (Entry 13E) — zero tax, zero withholding, subject only to prescribed information-reporting compliance to be notified by the Central Government.

What it does NOT cover: Listed equity shares, corporate bonds, REITs, InvITs, unlisted securities, or capital gains on indirect transfers. The equity and corporate debt capital gains architecture for foreign investors remains entirely unchanged.

The ordinance is significant, but its scope is deliberately narrow. It addresses a specific pain point — the cost of foreign participation in India’s sovereign bond market — at a moment when the rupee was under pressure and the government needed to signal commitment to the global fixed-income investor community that had recently brought India into the J.P. Morgan Emerging Market Bond Index. However, the broader framework governing capital gains tax on foreign investors in India, including the taxation of listed equities, corporate debt instruments and other investment assets under the Income-Tax Act, 2025, remains largely unchanged. It is reactive policy. What India now needs is proactive structural reform.

“The ordinance is good signal, poor strategy. Exempting G-Sec capital gains while retaining a 12.5% equity LTCG rate sends foreign capital exactly where India needs it least — into sovereign debt — and away from the equity markets that fund the private sector.” — TaxBizMantra Editorial View

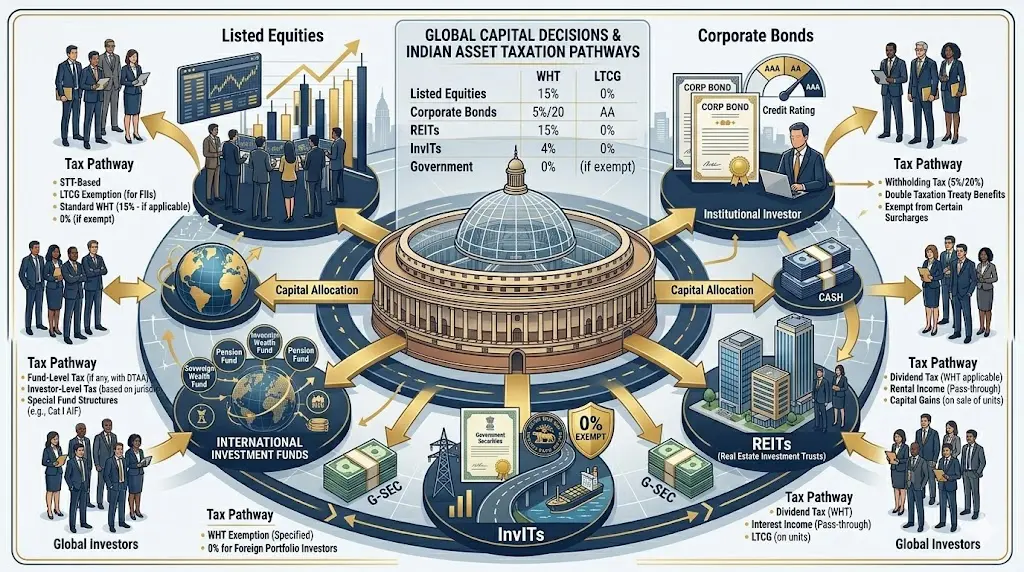

The Full Capital Gains Architecture for Foreign Investors Under IT Act 2025

Understanding where foreign investors stand today requires a precise map of the current legal provisions and their counterparts in the old Income Tax Act, 1961. India’s new Income Tax Act, 2025 (Act No. 30 of 2025), which came into force on 1st April 2026, uses entirely re-numbered sections. The capital gains rate provisions previously in Sections 111A, 112, and 112A of the 1961 Act are now in Sections 196, 197, and 198 of the 2025 Act respectively — a critical distinction practitioners must internalise.

| Asset Class | IT Act 2025 Section New | IT Act 1961 Section Old | Rate & Holding Period | FPI / FII Notes |

|---|---|---|---|---|

| Listed Equity Shares & Equity-Oriented MF Units — Long-Term | S.198, IT Act 2025 | Old S.112A (rate raised from 10% to 12.5% w.e.f. 23 July 2024 by Finance (No.2) Act, 2024) | 12.5% LTCG on gains above ₹1.25L; holding >12 months; no indexation; STT must be paid | Applicable to FPIs. No rebate under S.87A equivalent against this tax. |

| Listed Equity Shares & Equity-Oriented MF Units — Short-Term | S.196, IT Act 2025 | Old S.111A (rate raised from 15% to 20% w.e.f. 23 July 2024) | 20% STCG; holding ≤12 months; STT must be paid | Applicable to FPIs. Higher rate since Budget 2024 — key deterrent for short-term FPI flows. |

| Other Long-Term Capital Gains (listed bonds, debentures, unlisted equity) | S.197, IT Act 2025 | Old S.112 (restructured — 12.5% without indexation post-Budget 2024 for most assets) | 12.5% LTCG without indexation; holding >12 months (listed) or >24 months (unlisted equity) | FPIs taxed under S.210 on securities income. Corporate bonds: >12 months is long-term. |

| Government Securities — Interest & Capital Gains | Sch. IV, Entry 13D (FIIs) & 13E (BIS), IT Act 2025 — inserted by Ordinance No. 2 of 2026 | Previously: old S.115AD — 10%/20% depending on tenure; interest subject to TDS under old S.194LD at 5% (concessional) for FAR-eligible bonds | NIL — full exemption w.e.f. 1 April 2026 on both interest and capital gains. All tenures. | FIIs only (per S.210(6)(a) definition). BIS covered separately under Entry 13E. Reporting compliance required. |

| Income of FIIs from Securities (master provision) | S.210, IT Act 2025 | Old S.115AD — comprehensive provision covering FII income from securities, income other than dividends and interest from G-Secs | Rates as per S.210 table; effective 1 April 2026; read with Schedule IV exemptions for G-Secs | FPIs under SEBI FPI Regulations 2019 are notified as FIIs for S.210 purposes via Gazette notifications. |

| Sovereign Wealth Funds (SWFs) & Foreign Pension Funds — Specified Infrastructure Income | Schedule III, IT Act 2025 [equivalent to old S.10(23FE)] | Old S.10(23FE) — sunset extended from 31 March 2025 to 31 March 2030 by Finance Bill 2025. LTCG from unlisted debt also exempt. | NIL on specified income; minimum 3-year lock-in in infrastructure entities required | Applies to qualifying SWFs and Pension Funds only. Does not cover equity in non-infrastructure companies. |

| Indirect Transfer of Foreign Company Shares (India assets) | S.9, IT Act 2025 [Explanation 5 and related clauses] | Old S.9(1)(i) Explanation 5 — inserted by Finance Act 2012 post-Vodafone SC judgment; retro amendments later reversed for pre-2012 transactions | Taxable as deemed Indian income if Indian assets >₹10 cr and >50% of total foreign company assets | Significant concern for PE/VC funds, offshore holding structures and cross-border acquisitions. DTAA, PPT and GAAR considerations remain critical when evaluating indirect transfer exposure. |

| REITs & InvIT Units (Listed) | S.198, IT Act 2025 (for LTCG on units); distribution income per pass-through rules | Old S.115UA — pass-through treatment; LTCG on listed units at 10% pre-Budget 2024, now 12.5% | 12.5% LTCG on units held >12 months; interest distributions taxed at slab / treaty rate | Growing FPI interest in infra InvITs given the SWF exemption on underlying assets. |

* All rates exclusive of applicable surcharge and health & education cess of 4%. FPIs may claim DTAA benefits where applicable. IT Act 2025 effective 1 April 2026 (Tax Year 2026–27 onwards).

The Income Tax Act, 2025 (Act 30 of 2025) uses entirely new section numbers. The capital gains rate provisions practitioners cited for decades are renumbered as follows: old S.111A → new S.196 (STCG on equity, 20%); old S.112 → new S.197 (LTCG general, 12.5%); old S.112A → new S.198 (LTCG listed equity/MF, 12.5%). The DTAA relief provisions in old Sections 90, 90A, and 91 now correspond to S.159 of the IT Act 2025. GAAR provisions in old Sections 95–102 now correspond to Sections 178–184 of the IT Act 2025. Always verify the new section number before citing in returns, submissions, or legal opinions filed for Tax Year 2026–27 and onwards.

Section 210, IT Act 2025 is the master provision governing taxation of income of Foreign Institutional Investors from securities. It prescribes applicable rates on income other than dividends and interest from Government securities. It defines “Foreign Institutional Investor” by reference to Central Government notifications — which currently bring SEBI-registered FPIs under the 2019 FPI Regulations within scope. The term “securities” in S.210 carries the meaning in Section 2(h) of the Securities Contracts (Regulation) Act, 1956. The rates under S.210 are effective from 1 April 2026 and must be read with the exemptions carved out in Schedule IV, Entries 13D and 13E inserted by Ordinance No. 2 of 2026.

The Case for Abolition — Why the Status Quo Is Self-Defeating

The argument for abolishing capital gains tax on foreign investors is not a populist one, nor is it about favouring foreign capital over domestic savers. It is a structural economic argument with three distinct and verifiable planks.

1. The Competition Reality

India competes for global capital allocation in real time against jurisdictions that have permanently resolved this question. Singapore levies no capital gains tax on any investor — domestic or foreign — and its status as Asia’s premier financial hub is not unrelated to this policy choice. Hong Kong similarly imposes no capital gains tax. The UAE, Saudi Arabia, and a growing list of Gulf sovereigns are redesigning their tax architecture to attract institutional flows. When a fund manager in New York or London runs a model allocation across emerging markets, the effective after-tax return is a first-order input, not a footnote. A 12.5% LTCG rate on Indian equity under S.198, IT Act 2025 — layered on top of the Securities Transaction Tax, regulatory compliance costs, and currency hedging expenses — makes India’s real return profile materially less attractive than comparable ASEAN or Gulf allocations.

2. The Complexity and Compliance Cost

Beyond the rate, India’s capital gains framework imposes a compliance cost that is consistently underestimated in policy discussions. The distinction between FII and FPI classifications under S.210(6)(a), IT Act 2025 and the SEBI FPI Regulations 2019 is a source of recurring interpretive ambiguity. The interaction between the grandfathering clause for pre-January 2018 equity acquisitions, the revised holding period thresholds post-Budget 2024, and treaty override provisions under S.159, IT Act 2025 [old S.90/90A/91, IT Act 1961] creates a compliance architecture requiring dedicated tax counsel and measurable transaction costs at every entry and exit point. The indirect transfer provisions under S.9, IT Act 2025 [old S.9(1)(i) Explanation 5] — which continue to create uncertainty for PE/VC fund structures and offshore investment vehicles — remain a persistent overhang for multi-layered offshore vehicles. Smaller sovereign and institutional investors who lack dedicated India tax teams simply stay away. This is not a tax policy outcome; it is a tax architecture failure.

3. The Revenue Trade-Off Is Favourable

There is a reasonable counter-argument that abolishing capital gains tax on foreign investors sacrifices sovereign revenue. The data does not support this concern at meaningful scale. FPI capital gains tax collections have historically been a rounding error in India’s direct tax revenue — dwarfed by corporate tax, personal income tax, and the STT itself, which continues to apply regardless of capital gains treatment. What India loses in headline capital gains tax receipts, it more than recovers through deeper market liquidity, lower government borrowing costs (already demonstrably evident from the J.P. Morgan index inclusion), higher equity valuations benefitting domestic investors through market price-earnings expansion, and the real economy multiplier effects of increased FDI flows that follow financial market deepening.

“India’s direct tax receipts from FPI capital gains are not a meaningful revenue line. They are a meaningful deterrent line — and the two should not be confused in any honest policy discussion.” — TaxBizMantra Editorial View

A Proposed Framework — What Full Reform Should Look Like

A comprehensive capital gains tax reform for foreign investors does not need to be a binary all-or-nothing abolition. A tiered, conditionality-based framework can protect India’s policy sovereignty while dramatically improving its investment climate. The IT Act 2025’s clean Schedule-based architecture makes targeted reform surgically precise. Here is what the framework should contain:

Tier 1 — Already Done (G-Secs): Full exemption on G-Sec interest and capital gains for FIIs — Schedule IV, Entries 13D & 13E, IT Act 2025, w.e.f. 1 April 2026. Recommended extension: expand to all SEBI Category I FPIs explicitly via gazette notification under S.210(6)(a), removing definitional ambiguity.

Tier 2 — Zero LTCG on Listed Equity Held >24 Months: Amend S.198, IT Act 2025 [old S.112A] to introduce a 0% rate for qualifying FPIs holding listed equity beyond 24 months. This rewards patient long-term institutional capital — the kind India’s development agenda actually needs — while retaining the 20% STCG on short-term trades under S.196 [old S.111A] to discourage speculative volatility. Net effect: zero revenue cost on patient capital, preserved deterrent on hot money.

Tier 3 — SWF and Pension Fund Expansion: Amend the Schedule III equivalent of old S.10(23FE) to expand the qualifying investment universe beyond infrastructure to include manufacturing, climate infrastructure, data centres, and logistics — all currently excluded. Remove the sunset cliff (currently 31 March 2030); replace with a rolling 5-year renewal condition tied to deployment certification by DPIIT.

Tier 4 — Indirect Transfer Safe Harbour: Codify a statutory safe harbour within S.9, IT Act 2025 for fund-of-fund structures and offshore feeder vehicles where India assets represent less than 50% of total fund value — eliminating dependence on CBDT circular-by-circular relief that currently creates policy unpredictability for PE/VC investors at exit.

Tier 5 — GAAR Carve-Out for Commercially Substantive Structures: Amend S.178, IT Act 2025 [old S.95, IT Act 1961] to codify a statutory presumption that SEBI-registered Category I FPIs with at least 10 independent investors and genuine economic substance in the jurisdiction of incorporation will not be subject to GAAR invocation solely on the basis of treaty benefit claims — consistent with existing CBDT GAAR clarification circulars but now with statutory force.

The Counter-Arguments, Examined Honestly

Three objections are commonly raised against more aggressive capital gains reform for foreign investors. Each deserves a candid assessment.

Objection 1: “It Creates a Two-Tier System Discriminating Against Domestic Investors”

This is the most emotionally resonant argument, but it conflates two separate policy instruments. The domestic capital gains framework — 12.5% LTCG on equity above ₹1.25L under S.198, IT Act 2025, 20% STCG under S.196 — is designed with distributional equity and domestic savings mobilisation in mind. The foreign investor framework under S.210, IT Act 2025 is a different instrument serving a different goal: capital account deepening and market internationalisation. Most countries operate differentiated regimes for residents and non-residents without controversy. India already does this — the very existence of S.210 as a separate FII provision reflects this constitutional and policy principle. That said, any meaningful reform of the foreign investor framework should be accompanied by commensurate domestic relief — including raising the LTCG exemption threshold and restoring indexation on non-equity assets — so that the overall direction of tax policy rewards long-term investment across all investor categories.

Objection 2: “It Will Encourage Round-Tripping Through Treaty-Abuse Structures”

This was a legitimate concern under the old regime when treaty shopping through Mauritius and Singapore was rampant. The Multilateral Instrument (MLI), adopted by India and now reflected in renegotiated tax treaties, and the Principal Purpose Test embedded in most bilateral treaties have substantially closed this avenue. Anti-avoidance provisions under Sections 178–184, IT Act 2025 [old Sections 95–102, IT Act 1961 — GAAR provisions] further ensure that purely tax-motivated structures can be challenged. The CBDT has also clarified that GAAR will not be invoked where the jurisdiction of FPI is determined on non-tax commercial considerations and the main purpose is not to obtain tax benefit. The treaty-abuse objection is a reason for robust anti-avoidance rules — which India has — not for retaining capital gains barriers across all asset classes on all foreign investors.

Objection 3: “Revenue Foregone Must Be Compensated”

As argued earlier, the revenue numbers simply do not justify the structural deterrent effect. Any short-term revenue cost of capital gains reform would be substantially offset by higher STT collections as market volumes deepen, higher income from corporate tax as valuations grow and companies raise equity capital at lower cost, and improved GST collections from the real economy multiplier effects of increased investment. The fiscal argument for reform, properly modelled over a 5-year horizon, is strongly positive.

The IT Act 2025’s Structural Opportunity — Why Now Is the Moment

The Income-Tax Act, 2025 is more than a linguistic simplification of the 1961 Act. Its most important structural innovation for this policy debate is the Schedule-based exemption system: tax-free income is now listed in Schedule III and Schedule IV rather than scattered across more than a hundred sub-clauses of the old Section 10 and related provisions. The June 2026 ordinance is proof of concept: inserting Entries 13D and 13E into Schedule IV was legally and administratively cleaner than the equivalent amendment would have been under the 1961 structure. It also demonstrates how future reforms relating to capital gains tax on foreign investors in India could be implemented through targeted amendments without disrupting the broader framework of the Act.

This architectural clarity is precisely the opportunity India should use. A comprehensive Budget amendment to Schedule IV and Section 198 of the IT Act 2025, debated and passed in the Winter Session of Parliament, could deliver the full reform blueprint outlined above without requiring structural upheaval. The section numbers are new and already less encrusted with decades of litigation compared to their 1961 counterparts. The legal framework is in place. The policy question is whether the political will is ready to follow the legal architecture that now exists and modernise the broader regime governing foreign investor taxation in India.

Form 15CA / 15CB [unchanged from IT Act 1961 regime] — Required for remittance of capital gains proceeds outside India. Payer files Form 15CA online; CA certificate in Form 15CB required for remittances above ₹5L where a lower treaty rate is claimed. Applicable even after capital gains exemption, to document the nature of remittance.

Form 41 [new — replaces old Form 10F for Tax Year 2026–27 onwards] — Self-declaration by non-resident investors claiming DTAA benefits under S.159, IT Act 2025 [old S.90/90A/91]. Note: Form 10F continues for FY 2025–26 (AY 2026–27, i.e., income up to 31 March 2026). Form 41 applies from Tax Year 2026–27 onwards under the new Act.

Form 3CE [old Form 3CE — verify updated notification under IT Act 2025 rules] — Accountant’s report for royalty / fees for technical services transactions exceeding ₹1 crore; relevant for technology-heavy fund structures with management fee characterisation issues.

Prescribed Information-Reporting Form (To Be Notified) — The information-reporting requirement for FIIs and BIS to claim the Schedule IV, Entry 13D and 13E exemption under the June 2026 Ordinance. Exact form and manner of filing are yet to be notified by the Central Government; compliance with this requirement is mandatory as a condition of the exemption.

What FPIs and Their Advisors Must Do Right Now

Whether or not the broader reform agenda advances, the immediate compliance implications of the existing law changes are significant. Here is what foreign investors and their Indian tax counsel need to action in Tax Year 2026–27:

Verify FII notification status: The Schedule IV, Entry 13D exemption applies to FIIs as defined under S.210(6)(a), IT Act 2025 via Central Government gazette notifications. Confirm your fund’s SEBI FPI registration and that the applicable notification brings it within S.210 scope. Do not assume all FPIs automatically qualify.

Migrate treaty documentation to Form 41: Non-residents claiming DTAA benefits must use Form 41 (not Form 10F) from Tax Year 2026–27. Ensure Tax Residency Certificates from the home jurisdiction are current. Filing must be done electronically on the income tax portal before making any treaty-based withholding claim.

Reassess grandfathering positions on equity: The grandfathering rule for equity shares acquired before 31 January 2018 — preserving cost-of-acquisition based on FMV as of that date — continues under the IT Act 2025 framework through S.198. Ensure the FMV computation records are maintained and updated in your cost basis workings.

Await the Entry 13D/13E reporting form notification: The Central Government is yet to notify the prescribed form and manner for information-reporting required to claim the G-Sec exemption. Monitor the Official Gazette and CBDT notifications closely — the exemption is conditional on this compliance.

Frequently Asked Questions — Capital Gains Tax on Foreign Investors in India

Does the June 2026 Ordinance apply to all FPIs or only FIIs — and what is the difference?

The exemption under Schedule IV, Entry 13D of the Income Tax Act, 2025 (inserted by Ordinance No. 2 of 2026) applies specifically to Foreign Institutional Investors (FIIs) as defined under Section 210(6)(a) of the IT Act 2025 — which corresponds to the old Section 115AD(1) framework of the IT Act 1961. In practice, SEBI-registered FPIs under the 2014 and 2019 FPI Regulations have been notified as FIIs for this purpose via Central Government gazette notifications. However, not every SEBI-registered FPI automatically qualifies — it is essential to confirm that your fund falls within the specific gazette notification that designates it as a Foreign Institutional Investor under S.210. Category III FPIs, for instance, may need specific verification. The distinction between FII (as used in the IT Act) and FPI (as used in SEBI regulations) is a persistent source of confusion that practitioners must navigate carefully.

What is the LTCG rate on listed Indian equity shares for FPIs in Tax Year 2026–27?

For Tax Year 2026–27 (the first year under the Income Tax Act, 2025), the LTCG rate on listed equity shares and equity-oriented mutual fund units — where STT has been paid — is 12.5% under Section 198 of the IT Act 2025 (which corresponds to old Section 112A of the IT Act 1961, as amended by Finance (No.2) Act, 2024 w.e.f. 23 July 2024). The exemption threshold is ₹1.25 lakh of LTCG per financial year. Gains above this threshold are taxed at 12.5% without any indexation benefit. STCG on listed equity (holding ≤12 months with STT paid) is taxed at 20% under Section 196 of the IT Act 2025 (old Section 111A). Surcharge and health & education cess of 4% apply additionally.

How does a foreign investor claim DTAA benefit to reduce capital gains tax in India under the IT Act 2025?

Under Section 159 of the Income Tax Act, 2025 (which consolidates and corresponds to old Sections 90, 90A, and 91 of the IT Act 1961), a non-resident investor can claim the benefit of a Double Taxation Avoidance Agreement (DTAA) if it provides more favourable treatment than the domestic law rate. For Tax Year 2026–27 onwards, the investor must file Form 41 (which replaces old Form 10F under the new Act) along with a valid Tax Residency Certificate from their home jurisdiction, electronically on the income tax portal. The investor must also satisfy the Principal Purpose Test (PPT) and any Limitation of Benefits (LoB) clause in the applicable treaty, as strengthened by the Multilateral Instrument (MLI). GAAR provisions under Sections 178–184 of the IT Act 2025 (old Sections 95–102) can override treaty benefits if the arrangement is found to be primarily tax-motivated with insufficient commercial substance.

What does “Government security” mean for the purpose of the Entry 13D exemption?

For the purpose of Schedule IV, Entries 13D and 13E of the Income Tax Act, 2025 (as inserted by the Income-Tax (Amendment) Ordinance, 2026), “Government security” carries the meaning assigned under Section 2(f) of the Government Securities Act, 2006. This covers: (a) a security created and issued by the Central Government for the purpose of raising a public loan; (b) Treasury Bills; (c) Cash Management Bills; and (d) any other instruments notified by the Central Government under that Act. Importantly, State Development Loans (SDLs) — which are State Government borrowings — are not central government securities under the 2006 Act and would not fall within the Entry 13D or 13E exemption unless separately notified. Foreign investors in SDLs therefore remain subject to the standard capital gains and interest tax regime.

Are Sovereign Wealth Funds and foreign Pension Funds currently exempt from Indian capital gains tax?

Qualifying Sovereign Wealth Funds (SWFs) and foreign Pension Funds can claim exemption on specified income — including capital gains and interest — from investments in qualifying infrastructure entities and notified sectors under the provisions corresponding to Section 10(23FE) of the old IT Act 1961, now carried into the schedule of the Income Tax Act, 2025. Finance Bill 2025 extended the sunset date from 31 March 2025 to 31 March 2030. Capital gains from investments in unlisted debt securities of infrastructure entities are also exempt. Conditions include a minimum 3-year lock-in, the fund being wholly owned by the foreign government or central bank, and the investment being in a notified infrastructure company or NBFC-IFC. This exemption does not extend to equity investments in non-infrastructure companies, REITs (other than infra-focused InvITs), or corporate bonds of general companies.

What is the GAAR risk for foreign investors in India after the IT Act 2025?

India’s General Anti-Avoidance Rule (GAAR) provisions are now contained in Sections 178 to 184 of the Income Tax Act, 2025, corresponding to old Sections 95 to 102 of the IT Act 1961. GAAR applies to “impermissible avoidance arrangements” — those whose main purpose is to obtain a tax benefit and which lack commercial substance. For foreign investors, GAAR is most relevant where fund structures are established primarily in treaty jurisdictions to claim DTAA benefits with no genuine commercial presence. CBDT has clarified that GAAR will not be invoked where the jurisdiction of an FPI is determined on non-tax commercial considerations and the main purpose is not to obtain a tax benefit, and where any Limitation of Benefits clause in the treaty sufficiently addresses the avoidance concern. SEBI-registered Category I FPIs with genuine investor diversity and commercial substance face low GAAR risk in practice. The minimum tax benefit threshold for GAAR invocation is ₹3 crore.

Should India’s domestic retail investors be concerned that foreign investors may receive preferential capital gains treatment?

This is a fair and legitimate policy question. The short answer is that differentiated treatment is not inherently inequitable when it serves distinct policy objectives. The domestic capital gains framework — 12.5% LTCG under S.198 above ₹1.25L, 20% STCG under S.196, with STT offsets — is designed with distributional equity and domestic savings mobilisation in mind. The foreign investor framework under S.210 targets capital account deepening and market internationalisation. These are different instruments for different ends, and most comparable economies operate differentiated resident/non-resident regimes without controversy. That said, any meaningful reform for foreign investors should also be accompanied by domestic investor relief — particularly raising the LTCG exemption threshold materially, and restoring indexation on non-equity long-term assets — to ensure the overall policy direction rewards long-term investment across all investor categories rather than being perceived as favouring foreign capital over Indian savers.

The Bottom Line — India Cannot Afford to Think Small on This

The Income-Tax (Amendment) Ordinance of June 2026 is the most decisive signal India has sent to global fixed-income investors in years. It deserves recognition for its boldness — an emergency presidential ordinance to exempt G-Sec capital gains — even if its scope is deliberately limited. The question now is whether it remains an isolated measure or becomes the first step in a systematic overhaul of capital gains tax on foreign investors in India and the broader framework through which India taxes foreign capital.

India has the legal architecture it needs. The Income Tax Act, 2025 — with its clean Schedule-based exemption structure, its restatement of FII taxation under Section 210, its GAAR framework in Sections 178–184, and its DTAA provisions in Section 159 — gives Parliament and the executive the tools to extend, calibrate, and protect any capital gains reform without surrendering anti-abuse control. The economic case is compelling. The revenue trade-off is manageable over any serious modelling horizon. The competitive pressure from Singapore, the UAE, and a rapidly liberalising ASEAN is not theoretical — it is a live allocation decision made daily by fund managers across the globe.

What remains is political will, and a recognition that the new Income Tax Act, 2025 is not just a cleaner statute — it is a policy platform. India’s Amrit Kaal ambition of becoming a developed economy demands capital market depth that cannot be built on a tax architecture designed for a different era. The sections are renumbered. It is time for the policy to be rewritten too.

The June 2026 ordinance earns a qualified welcome — directionally correct, legally sound, and timely. But India’s ambition should not stop at G-Secs. A phased, treaty-consistent and GAAR-protected reduction to zero of capital gains tax on foreign investors in India, particularly qualifying long-term foreign equity investment, implemented through a Winter Session amendment to Schedule IV and Section 198 of the Income-Tax Act, 2025, could prove to be one of the highest-return fiscal policy decisions of this decade. The architecture is ready. The legal framework is already in place. The moment for reform is now.

Want more analysis on India’s Income Tax Act 2025 — NPS taxation, LTCG planning, FPI compliance, and DTAA strategy? Explore TaxBizMantra’s complete personal finance and tax coverage.

Read More on TaxBizMantra →Sources & References

-

Income-Tax (Amendment) Ordinance, 2026 (Ordinance No. 2 of 2026) – Official ordinance promulgated on 5 June 2026 inserting Schedule IV Entries 13D and 13E providing exemption for specified Government Securities income and capital gains earned by eligible Foreign Institutional Investors (FIIs) and the Bank for International Settlements (BIS).

View Official Ordinance PDF -

CBDT FAQs on Exemption to Foreign Institutional Investors (FIIs) in respect of Government Securities under the Income-Tax Act, 2025 – Clarifies the scope, eligibility conditions, reporting requirements and practical application of Entry 13D introduced by the Income-Tax (Amendment) Ordinance, 2026.

View Official CBDT FII FAQ PDF -

CBDT FAQs on Exemption to the Bank for International Settlements (BIS) in respect of Government Securities under the Income-Tax Act, 2025 – Clarifies the scope and operation of Entry 13E introduced by the Income-Tax (Amendment) Ordinance, 2026.

View Official CBDT BIS FAQ PDF - Income-Tax Act, 2025 – Relevant provisions discussed include Sections 9, 159, 178–184, 196, 197, 198 and 210, together with Schedule IV exemptions applicable from Tax Year 2026–27 onwards. View Income-Tax Act, 2025

- Government Securities Act, 2006 – Section 2(f) defining “Government Security” for purposes of the exemption framework discussed in this article. View Government Securities Act, 2006