- Why the right answer isn’t the same for everyone — and the one number that changes everything: your home loan interest rate.

- Real rupee-to-rupee comparison: what happens to ₹5 lakh invested in SIP vs prepaid into a home loan over 15 years.

- The new tax regime’s hidden impact on this decision — and why millions of Indians are getting it wrong.

- The 60:40 hybrid strategy that financial planners are recommending for salaried professionals in 2026.

- A decision framework based on your loan stage, risk appetite, and tax regime — with a clear verdict for each scenario.

Your bonus arrived. Your home loan is waiting. And your mutual fund SIP is whispering. Which one deserves your money more?

Every April and October, a version of the same question plays out across thousands of WhatsApp groups, financial planning sessions, and kitchen table conversations in Indian households: the annual bonus has landed, and nobody can agree on what to do with it. Prepay the home loan and sleep better at night, or invest it in a SIP and let compounding do its work over the next decade? It sounds like a simple choice. It is actually one of the most consequential financial decisions a salaried Indian will make — and most people make it based on instinct rather than numbers.

Loan rate below 8.5%? Invest the majority in a lump sum equity mutual fund. SIP returns historically outperform after tax.

Loan rate above 9.5%? Prioritise home loan prepayment. The guaranteed risk-free saving beats most fixed-income alternatives.

Loan rate between 8.5–9.5% (most borrowers in 2026)? Split it — 60% into an equity mutual fund, 40% as home loan prepayment requesting tenure reduction. This is the 60:40 hybrid strategy this article explains in full.

One rule applies in all cases: never deploy your bonus into SIP or prepayment until you have 6 months of expenses in a liquid emergency fund and adequate term insurance in place.

This article will give you the numbers behind each path. Along with the framework to make the right call for your specific situation, tax regime, and loan stage. Because here is the truth: both answers can be correct — just not at the same time, and not for the same person.

Understanding the Core Trade-Off: Guaranteed Return vs Market Return

When you prepay your home loan, you earn a guaranteed return equal to your loan’s interest rate. If your home loan is at 8.75% per annum, every rupee you prepay delivers a guaranteed, risk-free 8.75% annual saving — because you no longer owe interest on that principal. No market risk. No volatility. No waiting. It is the financial equivalent of locking in a fixed deposit at your loan rate, except it is even better because the savings are immediate.

When you invest the same bonus in an equity mutual fund SIP or lump sum, you are chasing a market-linked return. Indian equity markets — measured by the Nifty 50 — have delivered approximately 13% CAGR over the last 20 years. After accounting for Long Term Capital Gains tax (LTCG at 12.5% above ₹1.25 lakh per year), the effective post-tax return on equity over a 15-year horizon is typically in the range of 11–11.5%.

If your home loan rate is 8.75% and your post-tax SIP return is 11.2%, the SIP beats prepayment by 2.45 percentage points annually. On ₹5 lakh compounded over 15 years, that gap translates to approximately ₹18–22 lakhs more wealth from the SIP path — assuming returns stay consistent.

But if markets underperform — returning 9% instead of 12% — the SIP advantage shrinks to near zero. The guaranteed 8.75% prepayment return suddenly looks a lot more attractive.

This is the tension at the heart of the SIP vs home loan prepayment debate. The SIP has a higher expected return. The prepayment has a higher guaranteed return. Which matters more to you is a function of where you are in life, how risk-tolerant you genuinely are, and — critically in 2026 — which tax regime you have opted for.

The Tax Regime Factor Nobody Is Talking About

The 2025 Union Budget made the new tax regime the default for most salaried individuals — and this single change has quietly shifted the SIP vs prepayment calculation in a way most people have not processed.

Under the old tax regime: Home loan interest up to ₹2 lakh per year is deductible under Section 24(b). Principal repayment up to ₹1.5 lakh per year qualifies under Section 80C. This means a portion of your interest cost is effectively subsidised by the government — making the real cost of your loan lower than the stated rate.

Under the new tax regime (now default): Neither Section 24(b) nor Section 80C deductions are available. The effective cost of your home loan is exactly what it says on your statement. No subsidy. This makes prepayment more attractive — because the tax benefit of keeping the loan alive is zero.

Practical implication: If you are on the new regime with a loan at 9% or above, prepayment is delivering a better risk-adjusted return than most people realise.

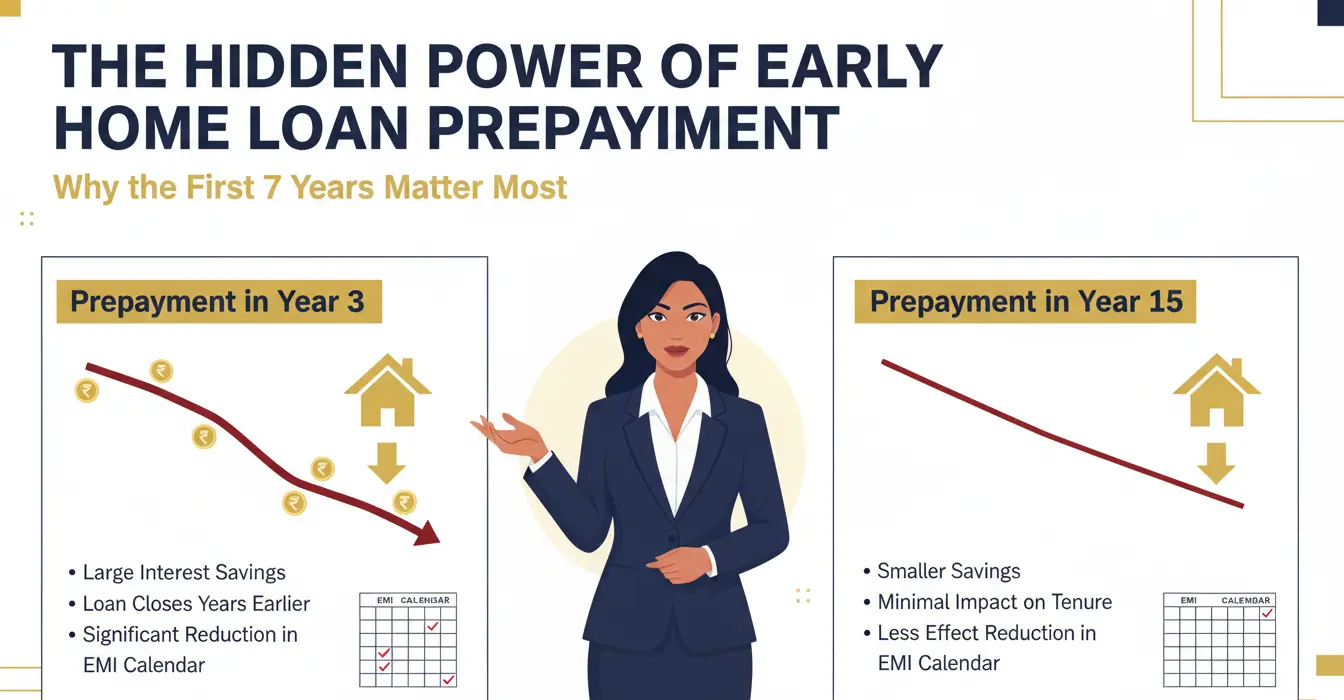

The Amortisation Secret: Why the Timing of Prepayment Changes Everything

Here is something that changes the entire calculation — and most articles on this topic gloss over it entirely. Not all prepayments are equal. A prepayment made in year 3 of a 20-year home loan is dramatically more powerful than the same prepayment made in year 15.

This is because of how home loan amortisation works. In the early years — typically the first 7 to 8 years — interest forms the majority of every EMI. On a ₹50 lakh loan at 9% over 20 years, your monthly EMI is approximately ₹44,986. In month 1, around ₹37,500 of that is pure interest and only ₹7,486 goes toward reducing your principal. By year 15, those proportions have reversed.

A prepayment of ₹5 lakh in year 3 of a ₹50 lakh loan at 9% saves approximately ₹18–20 lakhs in total future interest and closes the loan nearly 4 years early.

The same ₹5 lakh prepayment in year 15 saves only ₹3–4 lakhs in interest — because most of the interest has already been paid, and the remaining EMIs are predominantly principal repayment anyway.

Conclusion: If you are in the first 7 years of your home loan, prepayment’s return is dramatically higher than the headline interest rate suggests. SIP vs prepayment decisions must account for your loan stage — not just the interest rate.

Real Money: ₹5 Lakh Bonus — Comparing Both Paths Side by Side

Let us put real numbers on the table. Sanjay, 34, is a Pune-based IT professional with a ₹55 lakh home loan at 9% taken three years ago. He has an annual bonus of ₹5 lakh arriving this month. He is on the new tax regime. His question: SIP or prepayment?

| Parameter | Lump Sum in Equity SIP / MF | Home Loan Prepayment |

|---|---|---|

| Amount deployed | ₹5,00,000 | ₹5,00,000 |

| Return type | Market-linked (estimated 12% CAGR) | Guaranteed (9% = loan rate) |

| Value/Saving at 15 years | ~₹27.4 lakhs (pre-LTCG) | ~₹18–20 lakhs interest saved + 4 years less tenure |

| Post-tax outcome | ~₹25.2 lakhs (after LTCG 12.5%) | ₹18–20 lakhs (tax-free saving) |

| Risk | Market risk — returns not guaranteed | Zero risk — guaranteed saving |

| Psychological value | Wealth visible in portfolio | Debt burden reduces visibly each year |

| Liquidity | High — can redeem in 2–3 days if needed | Zero — money is locked into the loan, cannot be retrieved |

| Best suited for | Risk-tolerant, long-horizon investors | Stress-averse, early-stage loan holders |

In Sanjay’s case, the SIP path wins by approximately ₹5–7 lakhs on paper — but only if equity markets deliver their historical average. The prepayment path gives him certainty, reduces his loan tenure meaningfully (he is in year 3, the high-impact window), and eliminates the psychological weight of a large debt.

Given that Sanjay is 3 years into a 20-year loan at 9% on the new tax regime, both options are genuinely competitive. A pure SIP strategy is financially marginally better on expected returns — but a 60:40 split (₹3 lakh lump sum in equity MF + ₹2 lakh prepayment) is our recommendation. It captures wealth-building upside while meaningfully denting the loan in its highest-impact window.

When you receive an annual bonus, you have a lump sum — not a monthly surplus. Investing it all at once in an equity mutual fund is called a lump sum investment, which differs from a regular monthly SIP. Both have merit, but for an annual bonus specifically:

Lump sum investment deployed immediately captures full compounding from day one. It carries timing risk — if markets fall shortly after, you absorb the dip. A practical middle path: invest the lump sum in a liquid fund first, then trigger a Systematic Transfer Plan (STP) into an equity fund over 6–12 months. This averages your entry price without sacrificing time in the market significantly.

Your regular monthly SIP, funded from salary, should continue separately and independently of the annual bonus deployment. Never stop a running SIP to fund a lump sum investment.

The Decision Framework: Which Path Is Right for You?

Rather than a one-size answer, use this five-point framework to make the right call for your specific situation before your next bonus arrives.

One of the most common reasons people hesitate to prepay is the fear of penalty charges. Here is the definitive answer: for floating-rate home loans taken by individual borrowers, banks and NBFCs cannot charge any prepayment penalty — zero — under RBI regulations updated effective January 1, 2026.

This applies to all part-payments and full foreclosure on floating-rate loans. Fixed-rate home loans may still carry prepayment charges (typically 2–4% of the prepaid amount) — check your loan sanction letter specifically. If you are on a floating rate (which most borrowers are in 2026 after the RBI repo rate cycle), prepayment is entirely free. There is no financial reason to hold back on account of charges.

Also worth knowing: part payment of home loan vs full prepayment — you do not have to close the loan entirely. Most lenders accept part payments from ₹10,000 upward. Part payment reduces the outstanding principal and, if you request tenure reduction, significantly cuts total interest paid.

For most salaried Indians sitting in the 8.5–9.5% loan rate bracket — which is the majority of borrowers in 2026 — the debate often resolves itself through a simple hybrid: do not choose one over the other. Do both.

Allocate 60% of your annual bonus to a lump sum equity mutual fund investment (index fund or large-cap fund, not thematic or sectoral). This captures wealth-creation upside through compounding over a 10–15 year horizon.

Deploy the remaining 40% as a home loan prepayment — specifically requesting tenure reduction. This provides guaranteed interest savings, reduces your debt burden visibly, and takes advantage of the amortisation benefit if you are in the early loan years.

On a ₹5 lakh bonus: ₹3 lakh into equity MF + ₹2 lakh as prepayment. Review this split every 3 years as loan rates, market conditions, and your risk appetite change.

The psychological value of this approach is underrated. Markets will have bad years — the Nifty fell 23% in 2020 and investors who panicked and stopped their SIPs missed the 90% recovery. Having a simultaneous prepayment strategy gives you a tangible, guaranteed win each year, which makes it psychologically easier to stay disciplined with the SIP during market downturns.

The best financial decision is not always the one with the highest mathematical return. It is the one you can stick with for 15 years without abandoning it in the middle of a market crash or a personal crisis.

Your annual bonus is one of the most powerful financial tools a salaried professional has. It arrives once a year, it is a lump sum, and it can move the needle on both your debt and your wealth — if deployed with intention rather than impulse.

There is no universal answer to the SIP vs home loan prepayment question. But there is a framework: know your rate, know your loan stage, know your tax regime, and always protect your emergency fund first. If you are in the 8.5–9.5% interest rate bracket with 7 or more years remaining on your loan, the 60:40 hybrid strategy is not a compromise — it is the mathematically and psychologically optimal choice for most Indian households.

Stop treating this as an either/or decision. Your bonus is large enough to do both — and your financial future is important enough to make sure it does.

Use the calculator below to compare your estimated SIP wealth versus home loan interest savings based on your own bonus amount, loan rate, and investment horizon.

SIP vs Home Loan Prepayment Calculator

Compare estimated SIP wealth vs home loan interest savings using your annual bonus amount.

Your Estimated Comparison

Historical equity return references are based on long-term Nifty 50 index performance trends and publicly available mutual fund market data.

Home loan prepayment illustrations are based on standard amortisation calculations for floating-rate housing loans commonly offered by Indian banks and NBFCs.

Tax references relate to the new and old tax regimes under the Income Tax Act, including Sections 24(b), 80C, and 80CCD(1B).

This article is intended for educational and informational purposes only and should not be considered personalised financial, investment, tax, or loan advice.

SIP returns are market-linked and subject to volatility, while home loan prepayment outcomes vary based on loan tenure, amortisation schedule, lender terms, tax regime, and interest rates.

Please consult a qualified financial advisor, tax consultant, or loan expert before making major investment or prepayment decisions.

Similar Posts

SIP vs Real Estate in India (2026): Which Investment Creates More Wealth Over 20 Years?

A ₹10,000 monthly investment, 20 years, and two very different outcomes. Discover whether SIPs or property have historically created more wealth for Indian investors.

How to Build a Personal Budget That Actually Works

Tired of budgets that die by Day 10? India’s 4-bucket, 5-jar system tames UPI, automates SIPs, and brings calm to money—starting today

NPS Exit Rules Under New Tax Regime: ₹5 Lakh Rule, Annuity Trap & PFRDA 2025 Changes

Want to close your NPS account after the new tax regime removed the 80C benefit? Learn PFRDA’s 2025 exit rules, the ₹5 lakh threshold, annuity trap, and smarter alternatives including Section 80CCD(2).

Is NPS Withdrawal Taxable? Complete NPS Taxability Guide for 2026

NPS offers attractive tax benefits while investing, but how is the corpus taxed when you withdraw it? This guide explains NPS taxability, including maturity withdrawals, annuity income, partial withdrawals, death benefits, and the impact of the new 80% withdrawal rule.

NPS vs PPF: Which Is Betterfor Retirement Planning in 2026?

Everyone compares NPS and PPF on returns. Few compare what you’ll actually keep after tax. Here’s the retirement comparison every investor should read.

Rent or Buy House in India? Interactive Calculator + Real Financial Comparison

Should you buy a house or continue renting in India? Compare EMI, rent escalation, property appreciation, and long-term wealth creation using real financial scenarios and an interactive comparison calculator.