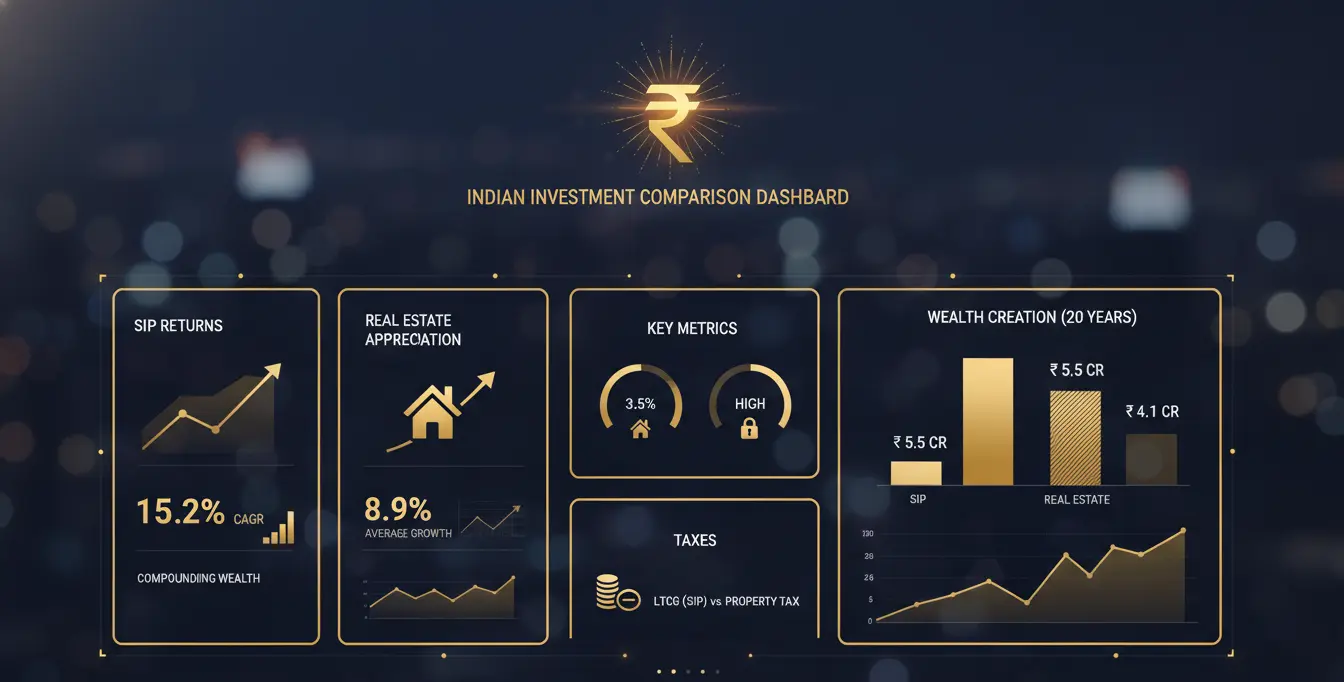

- 20-year return data: Nifty 50 SIP vs Indian residential real estate — the actual rupee corpus comparison most articles avoid showing.

- The hidden costs of property investment that quietly eat 2–3% off your real estate returns every year.

- Rental yield reality: what Indian cities actually deliver after vacancy, maintenance, and tax — versus SIP compounding.

- Tax efficiency in 2026: how the removal of real estate’s indexation benefit changed the LTCG comparison permanently.

- A clear, honest verdict — when SIP wins, when real estate wins, and what the wealthiest Indians actually do with both.

SIP vs Real Estate — What Happens to ₹10,000 a Month Over the Next 20 Years?

Rohan is 32, earns ₹18 lakh per annum, and has spent the last six months locked in the most exhausting internal debate of his adult life. His parents want him to buy a 2BHK in Sarjapur, Bengaluru — “property always goes up, beta.” His colleague Ankit has been showing him his mutual fund portfolio on his phone at every lunch, convinced that SIPs are the only intelligent answer.

The SIP vs real estate question is India’s most common long-term investment dilemma for salaried professionals — and Rohan is right to pause before answering it. Because both SIP and real estate can build wealth in India, but not equally, not always, and not for the same kind of investor.

This is the best investment in India debate that most financial content gets wrong — either cheerleading for equity markets or defending property with emotion rather than evidence. This article does neither. It puts both through the same honest lens: same rupee amount, same 20-year long-term investment horizon, post-tax, post-cost, post-everything returns. The goal is one thing — to answer definitively, with real data, which of these two assets builds more wealth for the average Indian investor over time.

For most Indian salaried investors with a 15–20 year horizon, equity SIP in an index fund outperforms direct residential real estate investment on total wealth creation, tax efficiency, liquidity, and minimum investment required. Real estate wins when you have leverage in a high-demand micro-market, need a forced savings mechanism, or are buying your primary residence. For pure wealth creation, the 20-year data consistently favours disciplined SIP investing — with the gap widening further after Budget 2024’s LTCG changes. This is a general educational overview. Individual outcomes depend on specific assets, timing, and personal financial circumstances. Consult a SEBI-registered investment adviser before making investment decisions.

SIP vs Real Estate — Setting the Ground Rules for a Fair Long-Term Investment Comparison

Before comparing SIP vs real estate in India, one clarification matters: this comparison is between investing in property (second home, investment flat) versus investing in equity mutual funds via SIP. Buying your primary home — the one you live in — is a lifestyle decision first and a financial one second. That is a different analysis, covered separately in our Rent vs Buy guide. For salaried professionals deciding between SIP and property as a wealth creation strategy, this is the article that runs the real numbers.

For this comparison, we use the following ground rules: ₹10,000 per month deployed consistently for 20 years, starting in 2004 and ending in 2024, in both an equity index fund SIP and a residential property investment in a major Indian city. We use verified historical data and account for all real-world costs — not just the headline numbers that make either asset look better than it is.

20-Year Returns: SIP vs Real Estate — Property Appreciation India vs Nifty 50

The Nifty 50 has delivered approximately 12–13% CAGR over the last 20 years (2004–2024, Total Return Index basis) — a genuine inflation-beating return that has significantly outpaced India’s average CPI inflation of 5–6% per year over the same period. There were significant crashes along the way — 2008, 2011, and 2020 — followed by recoveries that rewarded those who stayed invested. Wealth creation through SIP in India has been most powerful precisely because rupee-cost averaging forces consistent buying through those downturns. In the broader real estate vs stock market India debate, equity has the longer track record of outperformance — but Indian residential real estate across major metros has still delivered solid average property appreciation in India of 6–8% CAGR over the same period, with wide variation by city and micro-market.

Total invested: ₹24 lakh | Wealth created: ₹75.9 lakh

No brokerage, no stamp duty, no maintenance cost

Property value at end: ~₹96.7L | After interest (₹31L), stamp duty, maintenance & brokerage deducted

*Net equity retained after all real-world costs

The gap is significant — but what makes it even wider in real life is the cost structure of property investment, which most buyers never fully account for until after the purchase.

💰 SIP vs Property: Which Creates More Wealth?

Before investing in a flat or increasing your SIP, run a quick comparison. See which option could potentially create more wealth over the long term based on your own numbers.

Hidden Costs of Real Estate Investment in India That Silently Shrink Your Returns

When you buy an investment property in India, the stated purchase price is just the beginning. The true cost of real estate investment includes charges that collectively reduce your effective return by 2–3 percentage points every year — quietly eroding the property appreciation India headline figure that agents and developers advertise. Unlike a SIP in an equity fund, where the only cost is a 0.1–0.2% annual expense ratio, property investment carries a heavy cost structure at every stage: purchase, holding, and sale. And unlike a SIP, property returns are not automatically inflation-beating after these costs are deducted — particularly in slower-growth metros.

At purchase: Stamp duty and registration charges of 5–11% of property value (₹3–7 lakh on a ₹60 lakh flat). Brokerage of 1–2%. Interior fit-out for a rental property: ₹2–5 lakh typically.

Every year: Home loan interest — on a ₹48 lakh loan at 9% for 20 years, you pay approximately ₹58 lakh in interest alone, effectively doubling the cost of the property. Annual maintenance and society charges: ₹60,000–₹1.2 lakh. Property tax: ₹10,000–₹40,000 per year depending on city. Vacancy: 1–3 months of lost rent annually is realistic for most investor-owned flats.

At sale: Brokerage of 1–2%. LTCG tax at 12.5% without indexation benefit (Budget 2024 removed automatic indexation for properties purchased on or after July 23, 2024; pre-July 2024 properties may choose between 12.5% without indexation or 20% with indexation, whichever is lower). After all these costs, a property that appreciated at 7% annually often delivers an effective investor return of 4–5% — not the 7% headline figure that friends and family cite.

None of these costs apply to a SIP. The expense ratio of an index fund is 0.1–0.2% per year. There is no brokerage on purchase, no annual maintenance, no tenant management, and no stamp duty. The compounding works without friction — which is, in large part, why the 20-year corpus gap is as wide as it is.

Rental Yield and Passive Income from Property — What Indian Cities Actually Deliver

Property bulls often counter the returns argument with rental income. Fair point — rental yield is real money. But the rental yield reality in Indian cities is considerably less impressive than the “passive income from property” narrative suggests.

These are gross yields — before vacancy (deduct 0.5–1%), maintenance (deduct 0.3–0.5%), property tax (deduct 0.2%), and income tax on rent at your slab rate (deduct up to 0.9% at 30% bracket). Net rental yield after all deductions: 1.2–2.2% in most Indian cities. This is a real income stream — but it does not fundamentally change the wealth-creation comparison against a well-run equity SIP compounding at 12%.

Tax Efficiency in 2026: Why SIP Is Now the More Tax-Efficient Long-Term Investment in India

The tax treatment of SIP vs real estate changed significantly with Budget 2024 — and the change went almost entirely in favour of equity investors. Most articles have not updated their tax comparison. Here is the current picture.

Equity SIP / Mutual Fund LTCG: Gains above ₹1.25 lakh per financial year are taxed at 12.5% after 12 months of holding (long-term). Short-term capital gains (held under 12 months) are taxed at 20%. Redemptions can be staggered across financial years to keep annual gains below ₹1.25 lakh — making equity SIPs highly tax-efficient for disciplined investors.

Real estate LTCG — the current position after Budget 2024: A uniform 12.5% LTCG tax without indexation now applies to all properties. For properties purchased before July 23, 2024, owners have the choice of paying 12.5% without indexation OR 20% with indexation — whichever results in lower tax. For properties purchased on or after July 23, 2024, only 12.5% without indexation applies. The holding period to qualify for LTCG is 24 months. Importantly, the removal of automatic indexation significantly increases the taxable gain for properties held 10+ years — a meaningful change from the pre-Budget 2024 position.

Rental income: Taxed as regular income at your applicable slab rate — up to 30% plus cess (4%). A standard deduction of 30% on net annual value is available under Section 24(a), but rental income remains the least tax-efficient real estate income stream, particularly for those in the 20–30% tax bracket.

Net verdict on tax: equity SIPs are more tax-efficient than direct real estate in 2026 for most Indian investors — particularly for properties purchased after July 2024 where the indexation option is unavailable. Always consult a SEBI-registered advisor or chartered accountant for your specific situation.

Liquidity, Leverage and Life — Three Factors That Determine Which Investment Suits Your Financial Goals in India

Beyond returns and tax, three real-world factors separate SIP from real estate as a wealth-building tool — and they are the ones that matter most when life does not go according to plan.

Liquidity — the freedom to access your money: An equity SIP can be redeemed in 2–3 working days. An investment property in India takes 3–6 months to sell in good conditions, and may take 12–18 months in a slow market. During a medical emergency, a job loss, or a business opportunity, your SIP corpus is available. Your flat is not. This difference is not theoretical — it has real consequences for the 40% of Indian families who face at least one major financial shock per decade.

Leverage — the double-edged sword: Real estate allows you to control a ₹60 lakh asset with ₹10 lakh of your own money. If the property rises 10%, your return on invested capital is 60% — extraordinary. But leverage also amplifies losses and creates a fixed EMI obligation for 20 years. If your income drops — illness, layoff, business failure — the EMI does not pause. A SIP can be paused in 60 seconds. An EMI cannot.

Life flexibility — the cost of commitment: A 20-year home loan is a financial marriage. Salaried Indians in 2026 change cities more frequently than any previous generation. Selling an investment property to relocate means brokerage costs, tax events, and months of friction. A SIP portfolio moves with you, city to city, employer to employer, country to country — without a single form beyond a bank account update.

SIP vs Real Estate — Rohan’s ₹50 Lakh Decision with Real Rupee Numbers

Back to Rohan. He has ₹10 lakh saved and can invest ₹25,000 per month. Two paths:

| Parameter | 📈 Equity SIP Path | 🏠 Investment Property Path |

|---|---|---|

| Initial deployment | ₹10L lump sum + ₹25,000/month SIP | ₹10L down payment on ₹50L flat |

| Monthly commitment | ₹25,000 (fully flexible) | ₹45,000 EMI (fixed 20 years) |

| Upfront costs | ₹0 beyond investment | ₹3–4L stamp duty + registration |

| Asset value at 20 years | ~₹2.85 crore corpus (12% CAGR) | ~₹1.93 crore property (7% appreciation) |

| Total interest paid | N/A | ~₹58 lakh in loan interest |

| Net wealth created | ~₹2.61 crore post-LTCG | ~₹1.2–1.4 crore net of all costs |

| Liquidity | Full — 2–3 days | Very low — 3–12 months to sell |

| Flexibility | Pause, increase, redeem anytime | Fixed EMI for 20 years |

For Rohan, at 32, mobile in his career, and not buying a home to live in — the SIP path creates approximately ₹1.2–1.6 crore more wealth over 20 years while giving him full liquidity and zero EMI pressure. His parents are not wrong that property can build wealth. But the question was never whether property builds wealth — it was whether it builds more than SIPs. And on that question, the data in 2026 is clear.

The wealthiest Indian families do not choose between property and equity. They own both — but they build their equity corpus first, and buy property from a position of financial strength, not financial obligation.

Which Is the Best Investment in India — SIP or Real Estate? The Honest Verdict

- Your primary goal is pure wealth creation

- You are 25–40 with a 15–20 year horizon

- You value liquidity and flexibility

- You are on the new tax regime

- You cannot sustain a 20-year EMI safely

- You may change cities or countries

- You have investment discipline to stay in markets

- You want low minimum investment (from ₹500/month)

- You buy in a high-growth employment hub micro-market

- You hold commercial property with 6%+ yield

- You lack investment discipline — EMI enforces saving

- You have high conviction in a specific location’s demand

- You need a tangible asset for psychological security

- You are buying your primary home to live in

- You have 15+ year horizon in a stable city

- You can use leverage smartly without overextending

A note on REITs: For investors who want real estate exposure without direct property ownership, Indian REITs (Embassy REIT, Mindspace REIT, Brookfield REIT) offer an excellent middle path — distributing 90% of net distributable cash flows as dividends, fully liquid like stocks, and delivering 7–9% total returns without the stamp duty, EMI, or maintenance burden of direct property. REIT returns are not guaranteed and are subject to market risks.

The SIP vs real estate debate in India has a clear winner on most financial metrics in 2026 — and that winner is equity SIP, for most investors, over most long-term investment horizons. Whether your financial goal in India is early retirement, children’s education, or building a retirement corpus, the 20-year return advantage of equity SIP is real. The tax efficiency advantage has grown after Budget 2024, the liquidity advantage is permanent, and the minimum investment advantage is transformative for younger salaried Indians building wealth from scratch.

But real estate is not a failed investment. Leverage in a high-demand micro-market, commercial property with strong yields, and REITs for income — these are legitimate, powerful wealth-building tools. The wealthiest Indian families use both — equity for long-term compounding and flexibility, property for leverage and tangible security. The sequence matters: build your SIP corpus first, buy property from a position of financial strength, not financial desperation.

As for Rohan? He started a ₹25,000/month SIP last month. His parents are still sending him WhatsApp messages about a 3BHK in Electronic City. For now, the numbers are on his side.

The analysis, historical comparisons, and illustrative figures presented in this article are based on publicly available market data, regulatory publications, and industry research reports from the following authoritative sources:

- National Stock Exchange (NSE) — Nifty 50 Total Return Index (TRI) historical performance data.

- Reserve Bank of India (RBI) — Consumer Price Index (CPI) inflation and macroeconomic data.

- National Housing Bank (NHB) — RESIDEX residential property price trends and housing market statistics.

- Knight Frank India Research — Residential market and rental yield reports.

- ANAROCK Research — Indian residential real estate market studies and city-wise trends.

- Union Budget & Finance Act 2024 — Capital gains tax and indexation-related amendments.

Important: Historical returns and market data are provided for educational and illustrative purposes only. Actual investment outcomes may vary significantly depending on market conditions, property location, fund selection, investment horizon, taxation, and individual circumstances.