Download Freelancer Income Tax Calculator Excel under Section 44ADA for FY 2025-26 (AY 2026-27)

India’s most detailed Excel-based income tax calculator for freelancers and professionals under Section 44ADA. Compares New vs Old Regime, auto-checks 44ADA eligibility, calculates Marginal Relief, and tells you exactly which regime saves you more money.

This calculator is primarily designed for FY 2025-26 (AY 2026-27). Since Budget 2026 introduced no slab changes, the same calculator structure remains broadly applicable for FY 2026-27 (AY 2027-28) as well.

India’s freelance economy now includes over 15 million professionals — doctors, lawyers, CAs, IT consultants, architects, and content creators. Yet most of them either overpay tax by choosing the wrong regime, or underpay and face interest penalties later. One wrong decision costs between ₹20,000 and ₹80,000 every year.

The problem is not lack of intelligence — it is lack of the right tool. Most online income tax calculators for freelancers are built for salaried employees. They do not understand Section 44ADA, do not check the ₹50L vs ₹75L digital receipt threshold, do not apply age-wise old regime slabs, and certainly do not calculate Marginal Relief under the new regime.

That changes today.

Wrong Regime = Wrong Tax

Choosing New vs Old Regime without a proper comparison can cost ₹20,000–₹80,000 in avoidable tax every year.

44ADA Limit Confusion

The ₹50L vs ₹75L threshold depends on your cash vs digital receipt split — most freelancers don’t know this rule exists.

Advance Tax Mistake

Under Section 44ADA you pay advance tax in ONE installment by 15th March — not in four quarterly installments like others.

Download Free Income Tax Calculator Excel for Freelancers — AY 2026-27

📊 Income Tax Calculator — Freelancer & Professional

Section 44ADA Presumptive Tax | New Regime vs Old Regime | Finance Act 2025 | AY 2026-27

Works on Both Excel and Google Sheets

Open in Microsoft Excel 2016 or later for best experience. Google Sheets users may notice minor formatting differences — all formulas work correctly.

What Makes This Calculator Different From Every Other Online Tool?

There are hundreds of income tax calculators online. Most are built for salaried employees. This one is built specifically for freelancers and professionals under Section 44ADA — with features that no generic calculator provides.

| Feature | Generic Online Calculators | TaxBizMantra Excel |

|---|---|---|

| Works completely offline | ✗ | ✓ |

| Cash vs Banking receipt split for 44ADA | ✗ | ✓ |

| Live ₹50L/₹75L eligibility check | ✗ | ✓ |

| Age-wise Old Regime slabs (Below 60 / Sr. Citizen / Super Sr.) | ✗ | ✓ |

| Marginal Relief u/s 87A (New + Old Regime) | ✗ | ✓ |

| Regime recommendation with exact saving amount | ✗ | ✓ |

| Single-installment advance tax amount (15th March) | ✗ | ✓ |

| All 10 eligible professions reference list | ✗ | ✓ |

| Saveable, reusable, printable year after year | ✗ | ✓ |

| Surcharge correctly capped at 25% for New Regime | ✗ | ✓ |

Who Should Use This Freelancer Income Tax Calculator?

This calculator is built for Resident Individuals and Partnership Firms whose income falls under Profits and Gains from Business or Profession (PGBP) and who are eligible for the Section 44ADA presumptive taxation scheme — provided gross receipts do not exceed ₹75 Lakhs.

Medical Professionals

Doctors, Surgeons, Dentists, Physicians, Pathologists, Radiologists

Legal Professionals

Advocates, Lawyers, Solicitors, Legal Advisors, Legal Consultants

IT & Tech Consultants

Software Consultants, IT Advisors, Technical Consultants, Web Developers

Engineering & Architecture

Consulting Engineers, Structural Engineers, Architects, Urban Planners

Accountancy Professionals

Chartered Accountants, Cost Accountants (CMAs), Company Secretaries

Interior Designers

Interior Decorators, Space Planners, Interior Design Consultants

Film Artists (CBDT)

Actors, Directors, Producers, Music Directors, Singers, Lyricists, Cameramen

Management Consultants

Financial Advisors, Business Consultants, Authorised Representatives

Section 44ADA is NOT for everyone

Photographers, event managers, advertising professionals, traders, commission agents, electricians, plumbers, and tailors are NOT eligible for Section 44ADA. They should use Section 44AD (business) or regular taxation instead.

How to Use This Income Tax Calculator for Freelancers — Step by Step

You do not need any accounting knowledge. Just follow these 8 steps and the calculator does everything else automatically.

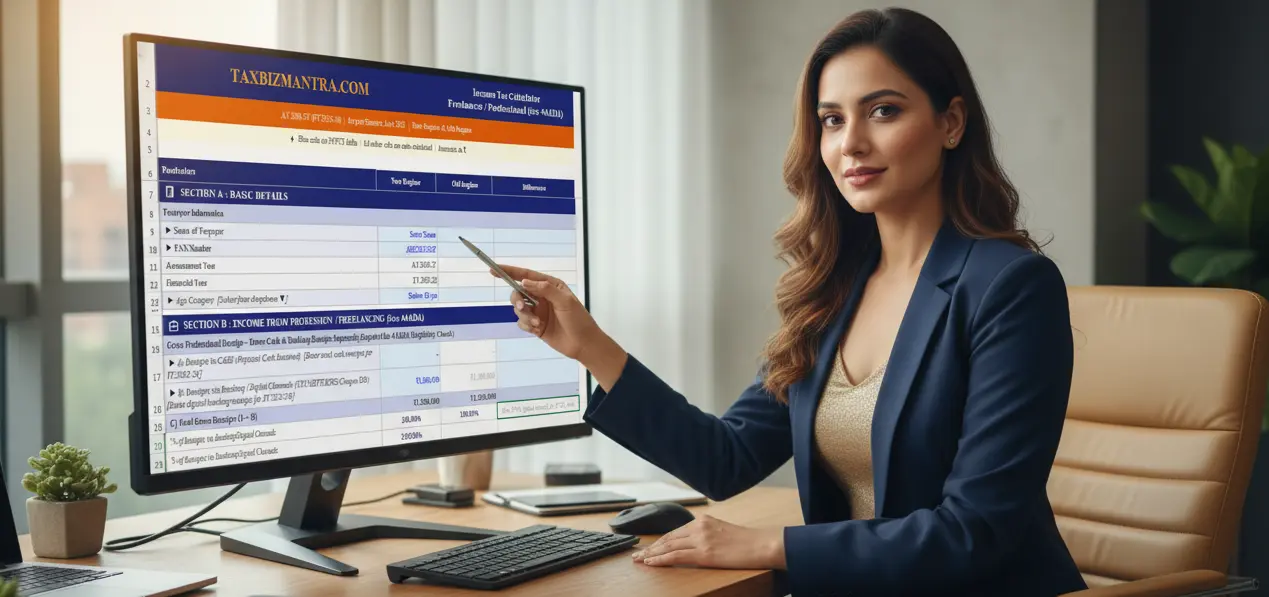

Download and Open the Excel File

Download the file and open it in Microsoft Excel 2016 or later. Enable macros if prompted. Go directly to the “📊 Tax Calculator” sheet — that is where you enter all your data.

Fill Section A — Basic Details

Enter your Name, PAN, and Age Category. The Age Category dropdown has three options: Below 60 yrs / 60-79 yrs / 80+. This is critical — it changes your Old Regime tax slabs automatically.

Enter Cash and Digital Receipts Separately

In Section B, enter your cash receipts (Row 17) and banking/digital receipts (UPI, NEFT, RTGS, Cheque — Row 18) separately for FY 2025-26. The calculator auto-computes the total and checks your digital receipt percentage.

Check the Live 44ADA Eligibility Alert

Row 21 shows a live eligibility status based on your total receipts and digital percentage. If it shows ⛔ INELIGIBLE, you cannot use this scheme and should consult your CA for regular taxation.

Add Other Income (Optional)

Enter any additional income — FD/savings interest, rental income, or any other income — in Section B rows 25–27. These are added to your presumptive professional income for both regimes.

Enter Old Regime Deductions (Optional)

For Old Regime only — fill your Chapter VI-A deductions in Section C: 80C (max ₹1.5L), 80D, 80E, 80GG, 80TTA etc. Under New Regime, these cells are automatically greyed out and set to zero.

Read Section G — Regime Recommendation

Section G shows a clear recommendation with both regime tax amounts and exact savings. Example: “New Regime is Beneficial — You Save ₹34,200 by choosing New Regime.”

Note Your Advance Tax Amount (Section H)

Section H shows your advance tax due amount for both regimes. Under Section 44ADA, pay 100% in ONE single installment by 15th March — not in four quarterly installments. Mark that date in your calendar right now.

Income Tax Slabs for Freelancers — FY 2025-26 (AY 2026-27)

As per Finance Act 2025, the following income tax slab rates apply for FY 2025-26 (AY 2026-27). Budget 2026 has confirmed no changes — these same slabs continue for FY 2026-27 (AY 2027-28) as well.

| Income Slab | Rate | Cumulative Tax |

|---|---|---|

| Up to ₹4,00,000 | NIL | ₹0 |

| ₹4,00,001 – ₹8,00,000 | 5% | ₹20,000 |

| ₹8,00,001 – ₹12,00,000 | 10% | ₹60,000 |

| ₹12,00,001 – ₹16,00,000 | 15% | ₹1,20,000 |

| ₹16,00,001 – ₹20,00,000 | 20% | ₹2,00,000 |

| ₹20,00,001 – ₹24,00,000 | 25% | ₹3,00,000 |

| Above ₹24,00,000 | 30% | ₹3,00,000 + |

| Income Slab | Below 60 | 60–79 yrs | 80+ |

|---|---|---|---|

| Up to ₹2,50,000 | NIL | NIL | NIL |

| ₹2,50,001 – ₹3,00,000 | 5% | NIL | NIL |

| ₹3,00,001 – ₹5,00,000 | 5% | 5% | NIL |

| ₹5,00,001 – ₹10,00,000 | 20% | 20% | 20% |

| Above ₹10,00,000 | 30% | 30% | 30% |

| Cumul. Tax at ₹10L | ₹1,12,500 | ₹1,10,000 | ₹1,00,000 |

Important: Finance Act 2025 vs Finance Act 2026

Finance Act 2025 governs FY 2025-26 (AY 2026-27). Finance Act 2026 governs FY 2026-27 (AY 2027-28). Budget 2026 confirmed no change in slabs. The Income Tax Act 2025 (effective 01 April 2026) replaces the IT Act 1961 with section renumbering only — tax rates are unchanged.

What is Section 44ADA? Complete Guide for Freelancers and Professionals

Section 44ADA of the Income Tax Act is a presumptive taxation scheme introduced specifically to simplify tax compliance for specified professionals. Instead of maintaining detailed books of accounts and proving every expense, you simply declare 50% of your gross receipts as taxable income — and the remaining 50% is presumed to cover all your professional expenses.

The Core Formula — Simple and Powerful

Regardless of your actual expenses, Section 44ADA allows you to declare:

Example: A freelance CA earns ₹30,00,000 in FY 2025-26. Under 44ADA, taxable income = ₹15,00,000 only — no matter what the actual expenses were. No books. No audit. No receipts required beyond invoices.

What is the Turnover Limit — ₹50 Lakh or ₹75 Lakh?

This is the most misunderstood part of Section 44ADA. There are two limits — which one applies to you depends entirely on your cash vs digital receipt ratio.

Banking/digital channels include: UPI, NEFT, RTGS, IMPS, Cheque, Demand Draft, Credit/Debit Card. Cash payments do not count. The calculator auto-checks this when you enter cash and digital receipts separately in Section B.

Can You Claim Deductions Under Section 44ADA?

This depends on which tax regime you choose:

- New Regime (Default): No deductions under Chapter VI-A (no 80C, 80D, HRA etc.). Taxable income = 50% of gross receipts + other income.

- Old Regime: Chapter VI-A deductions are fully available — 80C (₹1.5L), 80D, 80E, 80GG, 80TTA, 80G etc. To opt for Old Regime, file Form 10-IEA before the ITR due date.

One important note: you cannot claim additional business expense deductions beyond the standard 50% under 44ADA — even if your actual expenses are lower than 50%. The scheme works both ways.

Which ITR Form Should a Freelancer File?

Use when: Only professional income + salary/one house/other sources. Most 44ADA filers use this form.

Use when: Also have capital gains, more than one house property, or any foreign income/assets.

Advance Tax for Freelancers Under Section 44ADA — The Special Rule You Must Know

Advance tax is one of the most commonly misunderstood compliance requirements for freelancers. Most professionals assume they need to pay advance tax in four quarterly installments — June 15, September 15, December 15, and March 15. For most taxpayers, this is correct.

For Section 44ADA professionals, the rule is completely different.

100% Advance Tax in ONE Single Installment

Under Section 44ADA presumptive taxation, the entire advance tax liability must be paid in a single installment by 15th March of the financial year. The four-installment schedule does not apply.

This means for FY 2025-26, the due date is 15th March 2026.

🗓 Due Date: 15th March 2026 — 100% of TaxOther Taxpayers

4 Installments15 Jun / 15 Sep / 15 Dec / 15 Mar

15% / 45% / 75% / 100%

44ADA Professionals

1 Installment15th March only

100% of total tax

When is Advance Tax Applicable?

Advance tax is payable only if your total tax liability exceeds ₹10,000 in a financial year. If it is ₹10,000 or below, no advance tax is required. Non-payment or late payment attracts interest under Section 234B and 234C at 1% per month.

Frequently Asked Questions — Freelancer Income Tax India FY 2025-26

These are the most commonly searched questions about freelancer income tax, Section 44ADA, and this calculator. Each answer is written to directly address both your query and search engine AI summaries.

Taxable Income = 50% of ₹10,00,000 = ₹5,00,000

Under New Regime: Tax on ₹5,00,000 = ₹5,000 (₹5L – ₹4L = ₹1L × 5%). Less: Rebate u/s 87A (income ≤ ₹12L) = ₹5,000. Net Tax = ₹0 (Zero).

Under Old Regime (Below 60 yrs): Tax on ₹5,00,000 = ₹12,500. Less: Rebate u/s 87A (income ≤ ₹5L) = ₹12,500. Net Tax = ₹0 (Zero).

Both regimes result in zero tax for ₹10 lakh gross receipts under 44ADA. The TaxBizMantra calculator shows this automatically.

— New Regime is usually better for freelancers with income up to ₹24 lakh and limited deduction investments (small 80C, no home loan interest).

— Old Regime can be better if you have significant deductions: full 80C (₹1.5L), 80D (₹25,000+), home loan interest, NPS (₹50,000), etc. This requires income above a certain breakeven point where deductions outweigh the lower new regime rates.

The exact answer varies by age, income level, and deduction portfolio — which is precisely why this Excel calculator computes both regimes simultaneously and tells you the exact saving.

₹50 Lakh — Standard limit applicable when cash receipts exceed 5% of total gross receipts.

₹75 Lakh — Enhanced limit applicable when at least 95% of gross receipts are received through banking or digital channels (UPI, NEFT, RTGS, cheque, demand draft, credit/debit card). Cash receipts must not exceed 5% of total receipts to claim this higher limit.

If gross receipts exceed ₹75 Lakhs in any financial year, Section 44ADA is not applicable. The professional must maintain proper books of accounts and may be subject to tax audit under Section 44AB.

File ITR-3 instead if you also have: capital gains (equity, property, mutual funds), more than one house property, foreign income or foreign assets, or if you are a partner in a firm. Selecting the wrong ITR form is a common mistake — if in doubt, consult your CA.

1. Maintain proper books of accounts throughout the year

2. Record all income and expenses with supporting documentation

3. Get your accounts audited under Section 44AB by a Chartered Accountant

4. File ITR-3 (not ITR-4)

5. Pay advance tax in all four quarterly installments (not the single March installment)

The TaxBizMantra calculator auto-detects this and shows an ⛔ INELIGIBLE alert when receipts exceed the applicable threshold, so you are immediately alerted to seek professional guidance.

This calculator and the information on this page are based on the Finance Act 2025 and the Income Tax Act 2025 applicable for Assessment Year 2026-27 (Financial Year 2025-26). Budget 2026 has confirmed no changes to tax slabs for FY 2026-27. All figures are for estimation purposes only. Tax laws are subject to change. Please consult a qualified Chartered Accountant before filing your Income Tax Return. TaxBizMantra.com is not liable for any tax decisions made based on this calculator or the content of this page.

Sources: Finance Act 2025 | Income Tax Act | Section 44ADA, Section 44AA(1), Section 87A, Section 115BAC of the Income Tax Act | Income Tax Department | CBDT Notifications